Professor Rupert Read is Co-Director of the Climate Majority Project (CMP), and Co-Editor of the shortly forthcoming book THE CLIMATE MAJORITY PROJECT: https://londonpublishingpartnership.co.uk/climate-majority-project/.

PG: Your new book includes a chapter that you wrote specifically on the role of the insurance industry in relation to tackling our climate predicament. I’ve read it; it’s intriguing; it’s why we are having this conversation. So let me start by asking this question: Why a chapter on insurance rather than any other money pipeline, in your book?

RR: The insurance sector is a financial sector that is (or at least should be!) most fully aware of the existential threat posed by the climate crisis, since it directly impacts the sector’s economic success (and the extent to which it has been doing so has of course drastically accelerated over the last several years). Insurance industries/companies/entities currently have what I term anultimate double-bottom-line: where, as I’ll explain pretty fully in this interview, ethical practice simultaneously makes good long-term business sense. Some industry executives (and, notably, actuaries) are among the newly climate aware and are motivated to act from the perspective of their own values, coinciding with such enlightened self-interest. Joining the dots between climate and industry / key professions is a crucial communicative and organizing task of the Climate Majority Project (CMP), that I lead.

PG: So are you saying that Insurance has a critical role to play in gatekeeping bad actors, advocating policy changes, supporting climate initiatives?

RR: Insurers are powerful enablers and de facto gatekeepers to many highly extractive and destructive industries, from fossil fuels to air freight and intensive agriculture. They are party to not only the risks these industries face but also to those they create. As such they are in a position potentially to discriminate against harmful practices, penalizing those companies that pose the greatest risks to planetary health; and they can hope to emerge on the right side of history by doing so.

Insurance companies are (supposed to be) alive to risk: so, one risk they should be well aware of is the risk of their being sued in the future if they don’t take steps in this kind of direction. Another risk is that of consumer-boycott. Another risk is that of falling foul of conscious-quitting. My judgement is that all of those risks are likely to start to manifest significantly for – some – insurance companies within the next few years…

I am not saying insurance companies can do this all by themselves! But together they could; and especially if they got together to urge governments to regulate them such that they would have to… This is part of what I am calling for, Praveen. For insurers to think beyond the well-intentioned but inadequate UNEPFI framework, toward something that could work. Work with us in the CMP to figure out what regulations and incentives ought to be imposed upon insurance to help make it match-fit for a future. For co-creating an economy that will stop ever worsening our world, until (if present trends continue) there is no industry left.

PG: You are trying to mobilise the climate Majority, the majority of citizens who are now concerned. Insurance is not a remote ‘political’ or ‘activist’ concern. It is a concern of the climate majority; is that right?

RR: Yes, but to get to precisely why I need to take a step back.

I have spent much of my career working alongside the world’s leading climate scientists and ecologists. Their scientific papers are scary enough; but when one gets to ask them what they actually think, and feel – as I do – it is always worse than that. They are in deepening pain, over where collectively we are at. Moreover, the utterly unprecedented surface and (especially) ocean temperature rises of the last few months are taking us way further still into the danger zone. The world is right now moving rapidly into a state of two degrees C plus of global overheat; that is truly terrifying. Let me be unequivocally clear: this is the fight of – for – our lives. It’s not just about your children, it’s about how things could fall apart within the next 10-15 years.

CoP28 has done literally nothing to stop this trajectory.

Insurance must disclose what it knows about this dire threat. We need the world to know what insurers/actuaries etc. see in the risk and uncertainty that is ahead of us.

“Insurers sometimes assume that their business model is not badly affected by climate breakdown, because they can re-price premiums year on year”.

Moreover, and in a way more crucially still, just as the world at large faces an existential threat, so too does the sector of insurance, and sooner; as the world increasingly becomes uninsurable, insurance ceases to exist. AXA is famously on record as saying that the world is on course to become uninsurable, much of it perhaps by as soon as the middle of this century (and that estimate was made some time ago; the potential timeline for uninsurability has probably now come considerably closer). AXA are clearly not an activist group; they are primarily concerned with the continuation of their business. Just as AXA don’t need to be an activist group to align their values with combatting the climate crisis, neither does the average person. This is the philosophy of the Climate Majority.

PG: Insurance faces an existential risk. As the world increasingly becomes uninsurable. An uninsurable world has, by definition, no place for the insurance industry.

RR: That’s exactly right. A world of intensifying extreme weather and chronic climate impacts places unprecedented pressure on insurers in terms of claims, from business loss and property damage to crop failure. Conversely, escalating risk makes insurance unaffordable for clients and infeasible for insurers, depleting business for providers year on year.

The wider societal impact of climate and environmental damage will also have a knock-on effect on health, life expectancy and other types of claim. Transitional risks will impact insurers’ portfolios as assets are repriced. An increasingly volatile risk landscape threatens to destabilize business models that are founded upon what was historically a finite level of uncertainty and change; but it no longer is, now, in the ‘Anthropocene’. Increased frequency of acute outlier events – ‘thousand-year floods’, for example – causes the risk of bankruptcy to rocket. Re-insurers are already pricing this in, but they are of course ultimately the most vulnerable of all, in the sector. And in the difficult and desperate societal situation that we may be moving into, they should not assume that they are literally too big to fail (TBTF).

Insurers sometimes assume that their business model is not badly affected by climate breakdown, because they can re-price premiums year on year. But in the light of what I have just said, we can see that is ignorant and short-sighted. Unless the world changes course, insurance companies will either ungradually cease to exist because they will suddenly fail, or at best (!) they will gradually cease to exist, as their business simply disappears, as the world becomes uninsurable.

Is that the future you want for your profession?

So here is the deal: Help change the future, and become heroes rather than literally zeros.

PG: But what about ways in which insurance has tried to step up to the plate already. For instance: The Net Zero Insurance Alliance… would I understand correctly that it should in your view have been criticized for being too timid rather than too bold, in your view?

RR: Undoubtedly. As many readers will know, 2019 the Net Zero Insurance Alliance was set up under the auspices of the UN to transition members’ underwriting portfolios to net zero by 2050. The group’s ambition and scope were relatively limited, most obviously because the 2050 target is of course hopelessly late. If the Net Zero Insurance Alliance had been honest about the threat of the climate crisis, both to the world and their own fiscal future, then this target would have been set decades earlier.

Laughably, the NZIA was criticised by Republicans for being too activist. It has basically fallen apart under the criticism.

So a new start of some kind is needed, and more determinedly this time. Probably more bottom up, from within the relevant profession(s). Probably mostly ‘under the radar’ at first, to avoid getting targetted as the NZIA was.

The Climate Majority Project is interested in convening privately people from around and across the sector who would be interested in working together towards such a new start. I’ll develop this very practical point below.

“Insurance companies will have to be increasingly aware of their global reputation; a company that ignores the fuelling of the climate crisis will at some point before long worsen their results (their effects), and harm their reputation, perhaps fatally”.

PG: Regardless of the recent demonstration, in the failure of the NZIA, of craven short-term thinking from industry ‘leaders’, the climate predicament will not simply go away for insurers.

RR: Exactly. As economic damage from climate-linked events runs repeatedly into the tens and then hundreds of billions, insurers will be forced to consider how to invest in the benefits of mitigation and adaptation as part of their own survival strategy. The medium-long-term future of insurance is quite simply in extreme danger.

The reaction by the extreme Republicans against the Net Zero Insurance Alliance shows the (extreme) arrogance and stupidity that some members of our species exhibit to not recognize that their own survival is at stake. Well, our bet is that insurers etc. will turn out to be smarter than that. More precautious and wisely risk averse! Averse to the blatant risk of a sectoral suicide strategy – which is the current trajectory of insurance…

PG: What industry-shift in vision and long-term logic is urgently needed for steering the industry from its current catastrophe-course?

RR: I have already spoken about the incentive of insurance industries to act on climate (and similarly existential risks facing nature, and coming from AI, by the way, too) from a purely financial lens; as the climate deteriorates, insurance becomes impossible, and dwindles away. In addition to this, and as already hinted at above, insurance companies will have to be increasingly aware of their global reputation; a company that ignores the fuelling of the climate crisis will at some point before long worsen their results (their effects), and harm their reputation, perhaps fatally.

Insurance must also become more collaborative; either the entire sector will go down or it won’t. Only by sharing knowledge, discussing what works and what doesn’t, in ways that may be unfamiliar, does the sector stand a chance of surviving this existential crisis. The ‘anti-trust’ concerns that have been used to stymie such co-operation, especially in the USA, must be stood up to: there will be some sinking or swimming together. This is too big for any one company (however big!) to take on alone. (Though it is also worth noting, as I’ve already implied, that there are likely to be various kinds of negative effects on particular companies who lag in facing up to this great disruption, and various kinds of first-mover advantages to those that move to act so as to have a justified better reputation on climate, not to mention a smarter sense of what the risks and opportunities are in our changing world…).

PG: Will continuing to profit from harmful processes ultimately impact insurers’ public image, leading to a perceptible divergence between ethical and unethical insurers?

RR: Yes, that is what I mean. Failure to start doing the right thing will increasingly attract scrutiny and vocal (and litigious!) criticism from an increasingly powerful and broad-based climate movement; and experts who remain silent now will be judged harshly by publics suffering avoidable tragedies in years to come.

Obviously I have no crystal ball, but that much I can see.

If you want to get – to inhabit vicariously – a sense of how this could go well or badly, how it could play out, then read Kim Stanley Robinson’s cli-fi books, and Stephen Markley’s astonishingly brilliant book THE DELUGE. The latter develops a very believable picture of how pressure for change is going to build up, as the world climate crisis deepens.

PG: Do you really believe the climate movement and the insurance industry can be natural allies?

RR: Yes! Insurers are obliged to ‘model’ the future, and their capacity to assess and underwrite risk is as I’ve said contingent of course on a certain degree of predictability. An increasingly volatile risk landscape threatens to fatally destabilize business models that are founded upon a finite level of uncertainty and change. It really is therefore no great stretch of the imagination to see the climate movement and the insurance industry as natural allies.

And I mean this quite literally. The point of the Climate Majority Project is to make clear to the world that you don’t have to be an activist: you just have to act, where you have potential power and influence, for a future. For most people in insurance, that will mean: doing your job! But doing it differently. If you get busy doing that – and I will say more about just what that potentially amounts to, before this interview ends – then you are part of the climate majority. You are doing the world and your children proud – by potentially keeping the world insurable!

“I have spent much of my career working alongside the world’s leading climate scientists and ecologists. Their scientific papers are scary enough; but when one gets to ask them what they actually think, and feel – as I do – it is always worse than that. They are in deepening pain, over where collectively we are at”.

PG: What needs to change to keep the world insurable?

RR: To keep the world insurable, the climate crisis needs to be rapidly slowed. The insurance industry needs to step up and play its role in effecting this change. It can do this in the following four key ways, for starters:

- Tell the unvarnished truth about the climate dangers some/all customers are exposed to, now and over time. Insurance is how our civilisation deals with its vulnerabilities. Disclose what they – you – know about future rising risks and dangerous uncertainties that create these vulnerabilities. Do this in every way that is at your disposal. (If you encounter major obstacles in doing so, then consider leaking or whistle-blowing; for the future is at stake. But really this all ought to be doable in an open and co-operative manner. For we are talking here about a crisis which ultimately faces us all, as one.)

- Act without delay, using the levers at their – your – disposal to reduce the likelihood of those dangers, through choice of what they (you) agree to insure and at what price. For example, insurance for climate-destructive enterprises like fossil fuel extraction and fossil fuel funding should increasingly become punitively expensive or simply unavailable, helping to ‘strand’ those assets. On the other side of the ledger, offer incentives to those who take smart pro-climate action, both mitigational and adaptational. E.g. Reward businesses (with lower premiums) for having realistic, updated plans and protocols for dealing with climate risks such as supply-chain risks and disaster-risks.

- Place pressure on governments to reduce those dangers ‘at source’. This is absolutely critical. The lobbying power of insurers could be huge. Precisely because you are how our society processes and hedges against vulnerability. And because, as I’ve noted, you know: you know much of what is or may be coming.

- Put the vast funds accrued from premiums to work for the common good – i.e. strategic investment for a sustainable future and not just short-term, private profit – recognizing that such a future serves their (your) own long-term interests. Become impact investors, with your war-chests! Because, as Gandalf puts it at one key moment in Lord of the Rings: you may not realise it yet, but war is upon you. War is upon us. (If you are concerned that taking this bullet point on board might result in shareholder action against you, then become (say) a B-Corps, and/or lobby for the Better Business Act).

PG: What kind of Precautionary action is required by clients too?

RR: One thing clients can do is simply to voice their concerns and reservations. If one insurance company is ignoring the climate crisis, a client should instead approach a more responsible and far-sighted corporation, and then inform the original company why they no longer have your business. This will help impose climate-based thinking into the insurance industry.

The much bigger thing that clients should do is join the Climate Majority Project’s ‘Regulate us’ campaign. Business, except those businesses that need to cease to exist in order for there to be a future, has a common interest in governments setting a higher, level playing field, so that businesses can make a profit long term without driving the world over the climate cliff. In order for this to happen, business and finance needs to break cover from both free market fundamentalist dogma and ‘can-do’ ESG nonsense, and instead lobby governments, hard, to impose such a future-friendly policy environment. Before it is literally too late.

PG: Finally then, what do you want those in and around the insurance industry to do? Today?

RR: If you agree with what you have been reading here, then come and talk with us. You can email me at rupert@ClimateMajorityProject.com . We have already gathered together quietly a little group of industry insiders (and retirees). We want to build a community that will pursue the kinds of goals that I’ve outlined in this interview. And who are determined to realise them. Determined to be able to say that you are doing the right thing with your life and your power, at this critical moment for our world.

If that is you, then I can’t wait to hear from you.

PG: Many thanks Rupert for these meaty insights – a rare treat! My best wishes to the Climate Majority Project (CMP). Your success is critical for our planetary well-being and thereby the insurance industry.

https://www.linkedin.com/feed/update/urn:li:activity:7139979941772783617/

Thought leadership is an ongoing process that entails learning, refining, articulation and influencing. These call for curiosity, appetite, focus and perseverance. The challenges may lie within one or multiple components. Not all these rockets may fire simultaneously. A low motivation, for instance, might prove to be an underlying dampener. Health challenges like an emotionally charged environment, too. Information overload may impact the speed of processing relevant inputs. Fact checking may not always be straight forward. On the output side, if you are well ahead of time – the audience may not be ready or at best lukewarm.

Good thought leaders while aiming for consistent input and output have to be mindful of factors that may fuel any form of deficiency in this chain. Calibrate the process in ways that lift the game where control is possible thereby generate a high quality outcome. Whenever possible use a sounding board for an authentic feedback. If challenges persist, say a writer’s block, resulting slowdown could facilitate just the break you deserve.

Do keep it going!

The Journal, Chartered Insurance Institute

December 8, 2023

Delighted to share this abridged blog – https://lnkd.in/dXqarM82 – as re-published by The Journal, Chartered Insurance Institute.

#insurancebroker #ibai

illuminem

Illuminem.com

November 30, 2023

https://illuminem.com/illuminemvoices/the-baton-passes-on

This article is featured in illuminem’s Thought Leadership series on COP28 proudly powered by Tikehau Capital.

My Op-ed here features in illuminem’s Thought Leadership series on #COP28.

Will the front loading of ‘Loss and Damage’ at the COP mark a course correction in the ‘march of history’? It is a tacit agreement of the fact that the first world must own up to all the harm unleashed – upon what we now call #globalsouth – since the onset of industrial revolution.

A new world order powered by unambiguously clean sources of energy must address Climate breakdown, Bio-Diversity loss and Pollution that have besieged us.

The canvas must widen from shareholder to stakeholder, if the gravity and mindfulness must heighten. No amount of flooding, sea level rise or super storms can rid the micro-plastic that have begun to colonise human systems!

Can the insurance industry reimagine itself? What kinds of risks it must carry, what must it say no to, where must the float be invested without having to court sixth extinction?

The first ever workable break through comes from a collaborating specialty broker. Not sure if risk carriers realise they have been caught napping. That precisely presents an opportunity.

Triodos Bank has recently signed the treaty of the Fossil Fuel Non-Proliferation Treaty Initiative. Any guesses on who the first insurer could be?

In the meantime, look out for the ‘Island of Hope’ later this evening, at COP28, which will showcase “how risk capital markets can massively scale up funding for climate-vulnerable countries to create an essential pillar of Loss & Damage architecture”.

The Journal, Chartered Insurance Institute

November 28, 2023

When I was invited to write this piece for the Insurance Brokers Association of India (IBAI) – some months ago – the net-zero insurance alliance (#NZIA) implosion was a dominant thought. Global insurers abdicated an opportunity to own and address climate breakdown. Now this scorecard!

Is there another possibility? Could some international insurance broker/s take on the transformative role?

In a scenario where the fossil fuel industry was to strand – it could not only impair risk carriers but all those in the supply chain including intermediaries facilitating such a portfolio.

Apart from fossil fuel becoming history, Climate breakdown would deal a body blow to the current format of insurance both in terms of affordability and availability. Could Parametric be the new avatar? Any nimble player/s who may leverage such scale and complexity of disruption?

Cambridge Institute for Sustainability Leadership’s (CISL) new briefing – Risk sharing for Loss and Damage: Scaling up protection for the Global South offers a breakthrough in the design of the global architecture for Loss and Damage (L&D).

L&D in the international policy debate broadly refers to efforts to “avert, minimise and address loss and damage associated with climate change impacts, especially in developing countries that are particularly vulnerable to the adverse effects of climate change”. This blog provides a backgrounder.

It would use the economic efficiency of risk capital markets, which can convert modest annual flows from donors into major contractual entitlements for vulnerable countries when disasters strike, now and through to 2050.

Members of Howden Climate Parametrics modelled the technical cost and financial protection that could be achieved by using some L&D funds to access international risk capital markets. The action plan proposes to protect all 30 small climate vulnerable countries (population less than one million), from losing more than 10% of their GDP from climate shocks. It also advocated providing each L&D eligible country with $10m of annual premium to protect their highest priority needs.

The L&D domain includes Small Island Developing States (#SIDS), Least Developed Countries (#LDCs) and Vulnerable Twenty (#V20).

All this is happening outside the ambit of traditional insurance. The format does not entail a transactional relationship – always taken for granted. A broker facilitating an out of the box solution. Howden just took a significant first step. Is this a writing on the wall?

November 22, 2023

Illuminem.com

‘What happens when you put a fossil fuel exec in charge of solving climate change’ – screams a headline. The challenge is not about climate deniers alone. It is also an ever-evolving jargon and a seemingly never-ending analysis paralysis. Then there is a lot that believes something ought to be done but procrastinate. Caught in this bind, how do we move ahead? What will it take to break out of this inertia?

Twice this week we’ve seen the planet’s temperature briefly surpass 2 degrees Celsius above preindustrial levels for the first time in recorded history.

Over the last two years, as a backgrounder to the #COP, I have had the pleasure of hearing from outstanding upcoming women leaders. Focus being diversity and inclusion, given the serious gender bias. This time I had the privilege of speaking to renowned international leader Dr. Gillian Marcelle, PhD. She is super excited and keen to address the biggest existential crisis we have ever faced.

Gillian has vast experience in the design and implementation of blended finance strategies that often involve partnerships, #ecosystem strengthening and #designing architectures for #transformational change. At the helm of Resilience Capital Ventures (RCV) it is her endeavour to support efforts to restructure #internationalfinancialsystems in ways that benefit the #developingworld.

“Therefore, the relevance of COP28 UAE, in my view, is that these conferences continue to move the world forward by providing an albeit imperfect process of figuring out how to solve problems that extend beyond national boundaries”, says Gillian.

“This media and Western NGOs display a very different posture from the UK, where the Glasgow hosted COP26 was presented as the venue where the private sector would swoop in and take over climate finance. We all know how that turned out”, she cautions.

Gillian’s bold prescription: “Narrative change in finance and economics to place responding to the #polycrisis at the center of economic and investment strategies; movement building to tap into the knowledge of #climate and #social #justice advocates and activists around the world; and activating all forms of capital at scale with ecosystem strengthening efforts done in parallel”.

#Bridgetowninitiative

Mia Amor Mottley

Dr. Gillian Marcelle leads Resilience Capital Ventures LLC, (RCV), a boutique capital advisory practice specializing in blended finance. She has a proven track record in attracting investment and focuses on telecoms, fintech, renewable energy and regenerative agriculture. Her clients and partners include: The government of The Bahamas, MPC Energy Solutions, PolicyLink, Marin Agricultural Land Trust (MALT), AfricaBio and the Clinton Foundation. She currently serves on the Advisory Board of New Majority Capital and has guided numerous ventures in the role of Senior Advisor. Her specialty is the design and implementation of blended finance strategies that often involve partnerships, ecosystem strengthening and designing architectures for transformational change.

Gillian’s educational background includes earning degrees in Economics from the University of the West Indies, St Augustine, Trinidad & Tobago, and the Kiel Institute of World Economics, Germany; an MBA with a specialization in high technology management from the George Washington University and a doctorate in innovation policy from the Science and Technology Policy Research Unit, SPRU, University of Sussex. Her international public service includes appointments with the Global Building Network; several agencies in the United Nations system; World Economic Forum, Global Future Council on SynBio; and an appointment as a Commissioner on the Value Commission, a project of the Capitals Coalition.

PG: It is time for yet another COP. Do you see its ongoing relevance despite an oil-rich nation playing the host?

GM: The fact that the host of COP28 is the United Arab Emirates, a Gulf state country, has generated a lot of attention in the US and Europe and even calls for a boycott.

My country of origin is Trinidad and Tobago, an energy-led economy, and so simply from the point of view of hypocrisy, it would be silly for me to take a negative attitude towards the UAE.

Then there is this – the UAE is pursuing ambitious decarbonization and energy transition strategies as outlined in its National Determined Contribution (NDC) and the UAE Energy Strategy 2050.

UAE more than triple the share of renewable energy by 2030 to stay on track with its climate change mitigation goals, as well as help increase the share of installed clean energy capacity in the total energy mix to 30 percent by 2030.

The plans include:

…a broad range of measures including renewable and nuclear power, reverse osmosis desalination, improved efficiency, district cooling and demand-side management, carbon capture and storage (CCS), hydrogen use in industry, fugitive methane cutting, public transport and electric vehicles, innovative agricultural technologies, and others.

Source: Commitments and Contradictions: Gulf and Middle East Decarbonization Strategies Ahead of COP28. These efforts to make accelerated progress to reach net zero emissions by 2050 will be achieved by commitment of size-able investment with reported investments reaching USD 53 billion.

UAE has also strengthened its institutional apparatus in the following ways:

The UAE was the first Gulf state to announce a national climate strategy in 2017 and was also the first to link its climate strategy with its economic development plans, for which the UAE Green Agenda 2015-2030 was established as an overarching implementation framework. The UAE Council on Climate Change and Environment, established in 2016, is the committee responsible for overseeing the implementation of the Green Agenda. Source: The GCC and the road to net zero.

Moreover, the UAE has orientated itself in support of the concerns and negotiating demands of the developing world.

The relevance of COP28 UAE, in my view, is that these conferences continue to move the world forward by providing an albeit imperfect process of figuring out how to solve problems that extend beyond national boundaries.

The UAE supports green infrastructure and clean energy projects worldwide and has invested in renewable energy ventures worth around 16.8 billion USD in 70 countries with a focus on developing nations. It has also provided more than 400 million USD in aid and soft loans for clean energy projects. Source: The UAE’s response to climate change.

As part of its leadership role, the UAE through the COP Presidency has been active in offering support for the L&D Fund and led the way for standing up coalitions for accelerating renewable energy. Working with sixty countries including US, EU, South Africa and Vietnam among them, to make a high ambition pledge to scale down coal and triple investments in clean and renewable energy by 2030.

Notwithstanding all of these measures, commitments and policy advance, the UAE and other Gulf States face heavy criticism for maintaining and even expanding oil and gas production. It will be important going forward to monitor and hold accountable all fossil fuel providers with robust tax regimes, local supplier development initiatives and initiatives to invest oil and gas windfall profits in energy efficiency and accelerated rollout of renewable energy.

This media and Western NGOs display a very different posture from the UK, where the Glasgow hosted COP26 was presented as the venue where the private sector would swoop in and take over climate finance. We all know how that turned out.

As far as the relevance of the UNFCCC Conference of Parties negotiations go, many commentators, particularly those from the Global South, know that there is value to multilateral venues where the voices and votes of small and less powerful countries count.

Therefore, the relevance of COP28 UAE, in my view, is that these conferences continue to move the world forward by providing an albeit imperfect process of figuring out how to solve problems that extend beyond national boundaries.

I echo the views of Amb. Selwin Hart and the UN Secretary General in calling upon member states and non-state actors to use these opportunities well, to display more ambition and increase the proportion of adaptation finance.

For those very strongly concerned about the host of this year’s COP, they can wait until COP29 in Brazil to engage.

PG: Any thoughts on developed countries trying to push the L&D Fund out of the UNFCC? How and when does it become fully functional?

GM: My support for the L&D Fund is a matter of record. I saw the recent pieces regarding the recommendations of moving the secretariat out of the UNFCC.

Those of us concerned about establishing a mechanism to mobilize and deploy funds that compensate countries for cumulative and historical loss and damages arising from climate change regard any kerfuffle about bureaucratic arrangements as unnecessary delays.

When countries in the Global North wish to mount collaborative or national responses to natural disasters, wars, or pandemics, they find ways to proceed. Therefore, the agreement reached in early November were very welcome and set the stage for the Loss and Damages Fund to be on the official agenda.

Western media has, by and large, failed to cover this issue with balance and nuance. The road bumps are celebrated and presented as news without the corresponding long form investigative pieces to build commitment.

There are models of effective execution of large-scale financing that can be used as examples. It is also likely that the origin of the L&D Fund will have to be recognized if it is to have legitimacy. The scale of the financing required is certainly daunting.

As Avinash Persaud, advisor to Prime Minister Mia Mottley of Barbados, said when quoted in a recent Financial Times piece, progress on the L&D Fund should be regarded as a shared and important objective of the entire international community.

Western media has, by and large, failed to cover this issue with balance and nuance. The road bumps are celebrated and presented as news without the corresponding long form investigative pieces to build commitment.

There are very few journalists providing a sense of progress. As I have said before, “facts will not stop those who cannot drag their hearts and minds away from nomenclature wars and/or endless debates as to whether carbon taxes and voluntary initiatives work.”

The roll-your-sleeves-up-and-get-it-done community that is designing, deploying and evaluating solutions for the polycrisis should be amplified more. We are going to be using COP28 UAE as a focusing device for our efforts; A meeting place and venue for dialogue and knowledge sharing outside of the formal negotiations.

PG: The burgeoning Climate Crisis is defying all timelines and deserves urgent action. Aren’t there too many distractions getting in the way?

GM: I do not foresee any time soon where there will be no noise and distractions. In my view, what is required is: narrative change in finance and economics to place responding to the polycrisis at the center of economic and investment strategies; movement building to tap into the knowledge of climate and social justice advocates and activists around the world; and activating all forms of capital at scale with ecosystem strengthening efforts done in parallel.

What is required is: narrative change in finance and economics to place responding to the polycrisis at the center of economic and investment strategies…

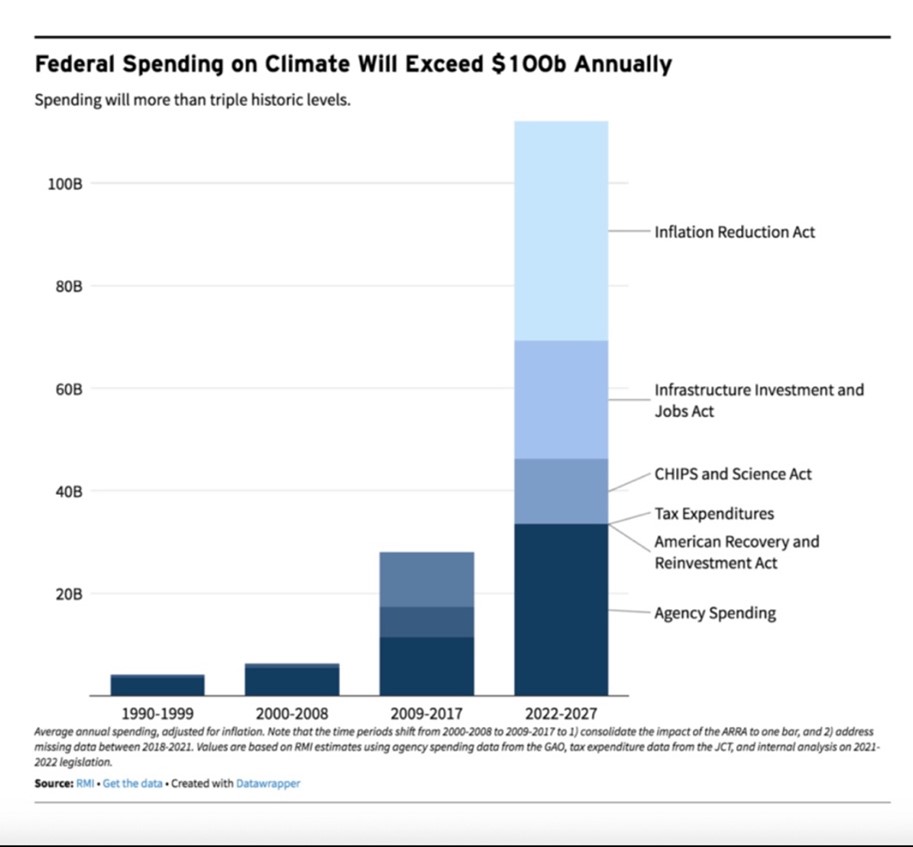

I am encouraged to see efforts along these lines in countries as diverse as Uruguay, where 98% of all energy is derived from renewable sources, and the United States, with billions in annual federal spending on climate under the Biden-Harris Administration.

Figure 1: U.S. Annual Federal Spending on Climate (1990-2027)

Source: RMI

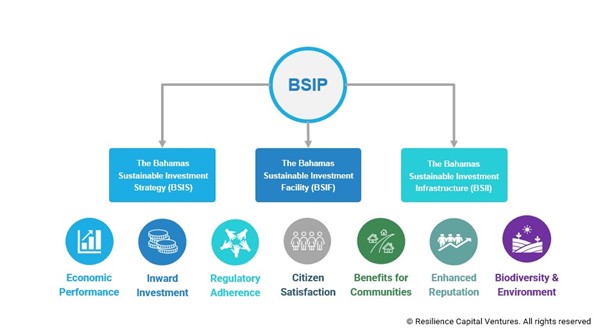

PG: Would you please share what ‘The Bahamas Sustainable Investment Program (BSIP)’ is about?

GM: The Bahamas Sustainable Investment Program (BSIP) is an ambitious multi-year investment and economic development program. BSIP seeks to position The Bahamas at the forefront of sustainable investment trends and deliver socio-economic benefits to the people of the country in line with national development goals and existing commitments on climate change and environmental response. This initiative is important for delivering on the government’s vision of a transformed economy and society.

Figure 2: The BSIP Overview

Source:The Bahamas Sustainable Investment Program

Once implemented, the BSIP will mobilize high-quality investments that produce risk-adjusted returns and positive social impact while adhering to global ESG standards and sustainability philosophies. This initiative will position The Bahamas as an even more attractive investment destination to global investors and align the domestic investment policy framework with global trends. Powered by the BSIP, The Bahamas will become a demonstration site showcasing what is possible when astute government leadership directs institutional development and facilitates private sector investment.

PG: What would be the role of Resilience Capital Ventures and how do you propose to address sluggishness in capital growth and reduction of misallocation decisions?

GM: The BSIP is designed by Resilience Capital Ventures (RCV) and we lead its execution on behalf of our client – the government of The Bahamas. This program serves to accelerate investment in mitigation, adaptation, and disaster management. By bringing together professionals skilled in capital markets, risk management, issuing securities, underwriting and placement, the program focuses attention of global capital markets on an underserved market. This is critical for success. Our focus draws on the dynamism of private sector firms in light of the many challenges that Development Finance institutions, quasi-public funds, and Multilateral Development Banks have with sluggishness and long lead times for deployment. Even the new President of the World Bank Group has taken aim at unnecessary bureaucratic processes as part of his plan for improvement.

Misallocation decisions arise out of gaps between actual and perceived risks and low levels of contextual knowledge and experience.

In my view, misallocation decisions arise out of gaps between actual and perceived risks and low levels of contextual knowledge and experience. Financiers take the easier and more familiar investment opportunities first. This means they rarely get to small islands in the Caribbean. This is not because of the inherent value, attractiveness, or necessity but simply because these jurisdictions are not top of mind.

Our approach draws on my pioneering experience in taking African telecom companies to global capital markets and more recent experience in helping private equity clients raise capital for renewable energy projects. My own experience is complemented and enhanced by a senior team with decades of experience and a track record of accomplishment. RCV is fortunate to have retained an entire bench of finance and development professionals, including members of the Diaspora, who are frankly fed up with the mediocrity that gets presented to governments in our countries of origin. We know that this is not the best in class and now have an opportunity to demonstrate what is possible and are putting accountability for our outputs up for scrutiny.

PG: Is there a synergy with the Bridgetown Initiative?

GM: It is possible for small island nations in the Caribbean to innovate in multiple directions at the same time. Our work on The BSIP is focused on the design and execution of capital market solutions and therefore, in alignment with and additional to the recommendations of the Bridgetown Initiative.

The articulate advocacy of Prime Ministers Philip Davis of The Bahamas and Mia Mottley of Barbados has raised the profile of the Caribbean at a time when this is sorely needed. However, it is important that no initiatives are pitted against each other because of intellectual laziness or lack of familiarity.

We at Resilience Capital Ventures are supportive of all efforts to restructure international financial systems in ways that benefit the developing world. We also join others in commending the leadership of Barbados in spearheading those efforts.

Praveen, thank you for the opportunity to share these views as the international community gets ready for COP28 in Dubai. With the conflict and war in the world, it is very important to focus on ways that we can move forward towards desired future states where humans and other species thrive and we do a better job of stewarding planet Earth.

PG: It is a real pleasure, Gillian. Many thanks for your unique insights and perspective. My best wishes in all your endeavours.

Republised by The Insurance Times

November 2023

Continued…

Alison Taylor is a clinical associate professor at NYU Stern School of Business, and the executive director at Ethical Systems. Her previous work experience includes being a Managing Director at non-profit business network BSR and a Senior Managing Director at Control Risks. She holds advisory roles at VentureESG, sustainability non-profit BSR, Pictet Group, and Zai Lab, and is a member of the World Economic Forum Global Future Council on Good Governance.

She has expertise in strategy, sustainability, political and social risk, culture and behavior, human rights, ethics and compliance, stakeholder engagement, anti-corruption and professional responsibility. Her book Higher Ground: How Business Can do the Right Thing in a Turbulent World will be published by Harvard Business Review Press in February 2024.

Alison received her Bachelor of Arts in Modern History from Balliol College, Oxford University, her MA in International Relations from the University of Chicago, and MA in Organizational Psychology from Columbia University.

Praveen Gupta: “Corporate America is finding itself trapped between society’s progressive impulses, and the conservative backlash”?

Alison Taylor: This is certainly true. But I think it’s been a long time since the world saw America as a role model. Lots of people still want to live here, for the economic opportunity and dynamism. But whether it is guns or reproductive rights, America has plenty of issues that make it a poor role model.

PG: What do you see in the crystal ball?

AT: Gosh I have no idea. The next election is terrifying. Clearly we are past the era of globalization and in a much more fragmented, contentious, fraught period where commitments to democracy seem increasingly fragile

PG: Why is delivering on both profit and purpose getting increasingly complex?

AT: I think it’s always been complex. One challenge is that no one agrees on what “purpose” actually is. Another is that doing the right thing, or even just focusing on environmental and social issues, is sometimes profitable, sometimes not. Timeframes, and investing for the long term in an unpredictable world, further complicate things. A final problem is that corporate value itself has become more intangible and perception based. It has reached the stage where we can’t even agree on terminology, let alone discuss the actual problems.

Recruiters want more international backgrounds, more career variety, more sustainability knowledge, better social skills, humility, and understanding of influence, not just barking orders from the top.

PG: A quieter leadership cohort in favor of collaboration and humility remains a minority vis-à-vis Silicon Valley god/emperor model?

AT: One point a smart reader of my upcoming book (see here for more details: https://www.amazon.com/Higher-Ground-Business-Right-Turbulent-ebook/dp/B0BTMRCCC1) made is that often this new generation of quieter leaders are just fronts for the existing founders and shareholders, who are now all neatly moving themselves into “executive chair” roles. But, notwithstanding that, there is recruitment data showing that what we are looking for in senior leaders is changing. Recruiters want more international backgrounds, more career variety, more sustainability knowledge, better social skills, humility, and understanding of influence, not just barking orders from the top.

PG: Milton Friedman’s compelling case for maximizing profit still prevails. Shouldn’t business schools be addressing this?

AT: I am not sure I agree. Businesses must make a profit to survive. Very few of the younger students I teach think that business exists solely to make a profit. To borrow a line from my book, humans need hearts to survive, but don’t exist solely to act as vehicles for their beating hearts. There is an expectation that business should treat workers properly and clean up its own mess. And interestingly, that position is not particularly partisan.

Many of the most powerful faculty continue to approach these questions in a way that might be argued is anachronistic.

On business schools, many of the most powerful faculty continue to approach these questions in a way that might be argued is anachronistic. I think the important thing is to not insist that professors parrot a certain worldview, but to open up the space for scrutiny and debate. We can disagree and debate ideas, that’s what a university is for.

PG: Wasn’t it Friedman who unleashed forces of corporate greed leading us down the path of Climate Breakdown?

AT: The problem is not so much Friedman but how he has been interpreted. Perhaps he was right IF there is a clean and clear line between business and politics. There isn’t.

PG: Does it make sense to continue treating branding, culture, sustainability, risk, and ethics as separate disciplines?

AT: My book is about why it does not.

PG: Moreover, performance matrices have little room for ethics?

AT: Some performance matrices consider not just whether a target was achieved, but how it was achieved. High performing assholes are the big vulnerability in a lot of organizations, not least because this encourages kick down/kiss up behavior.

In my book I recommend grounding a corporation’s ethical commitments in its impact on human beings.

PG: A deep global hunger for inspirational leadership prevails. Why are business schools unable to address the scarcity in moral leadership?

AT: I don’t know if business schools exist to teach moral leadership, and at least at Stern, there is quite a bit of focus on helping students to be better, more effective and ethical leaders.

One issue that is frequently raised is that personal and organizational ethics are not the same thing, and we are in a highly contentious and polarized era. In my book I recommend grounding a corporation’s ethical commitments in its impact on human beings.

Exercise practical curiosity about this, treat people with dignity and respect, make your best possible effort to do no harm and clean up your own mess. Interestingly, none of this is partisan and all of it is in line with how society would like business to behave!

PG: It’s been a real privilege tracking the evolution of your book and I am amazed how you draw in all the rapid-fire unravelling. Truly compelling. My best wishes for the upcoming launch, Alison!