Twelve years of association with a city is quite a time-frame. As a visitor over these many years – Seattle has kind of quietly grown within me. The Emerald city has all the energy, charm and passion that is bound to stir up emotions uniquely ones own. Could that be broken down into some form of algorithm? No way!

Over these years what has one seen not change or has indeed changed seems a tempting approach to take. And the downtown for me is essentially the focal point. So, the Yellow Leaf Cupcake Company continues to flourish. Looks like Studio Bad Animals, from across the road, must move on thanks to a proposed redevelopment. By the way the Emerald City seems to be the fastest growing in all of the USA. It has the highest number of operational cranes – perhaps more than all the resident sea gulls.

Whole Foods got acquired by locally headquartered Amazon with its recent landmark globe shaped entrance – truly has its global design in play. The takeover almost coincided with the demise of Sears. Owners of Kmart a pioneer of the retail revolution, an original favourite since my first visit to America. RIP Paul Allen. Virtually seems like he was the force behind everything visionary that has happened here.

Sights, sounds & the vibrancy!

The first ever Starbucks at 1912 Pike Place remains as busy as ever. Finally it has a foothold in India and is well past 100 outlets. Seattle averages one store for every 4000 people! Fall seems no different from summer when it comes to action around the Farmer’s Market at the Pike. It’s the artists, musicians, vegetable, flower and fruit vendors and a whole lot of diverse food that can keep you hooked all day long. I am told people drive from Vancouver to savour the Piroshky offerings. The Pike Place Fish Company can never be short on drama.

Of course I do hear murmurs on how expensive the city has become particularly for artists and teachers. That is not good news though. Uber is finally a settled mode of mobility after years of protests by the yellow taxis. And with some luck you might run into good artists doubling as Uber drivers. I guess that applies to other equally fast growing cities like Austin (Tx), as well. A fall visit tends to keep you more indoors, thanks to the cooling weather, thus more time to interact with artists. Mya Kerner shared brilliant insights into her masterful devotion to mountains. Her paintings bring a rare grandeur into living rooms.

Let there be Music!

The range is truly phenomenal. Be this the prancing violinist at the Space Needle or the duo who play the piano and violin at the Pike Place – they are all outstanding entertainers. The masters of Western Classical or Jazz give you the uplifting experience at the likes of the Benaroya Hall and the Seattle Art Museum. Behzod Abduraimov, the Uzbek genius who started playing piano at the tender age of of five, recently mesmerised the audience with his phenomenal technique and breathtaking delicacy. His magical fingers were such a delight to watch as he played Beethoven’s First Piano Concerto. Thomas Dausgaard the renowned conductor gave glimpses into his virtuosity and what one might expect from the conductor in residence at the Seattle Symphony, effective 2019.

Earshot Jazz Festival, currently ongoing, is an outstanding showcasing that Seattle can take pride in. It’s Mission Statement says it all: To ensure the legacy and progression of the art form, Earshot Jazz cultivates a vibrant jazz community by engaging audiences, celebrating artists, and supporting arts education. Listening to the sparkling Tom Harrell Quartet was magical and the time just zipped past. Apart from the legendary trumpeter Tom himself were his regulars Ugonna Okegwo (bass) and sensational Adam Cruz (drums). They were joined by brilliant next-wave Cuban pianist David Virelles. Also performing in the course of the event is a Cuban all women’s band. A stunning four weeks of exotic musical treat making Seattle an irresistible Jazz destination!

City of Literature!

Quoting author and editor Ryan Boudinot ‘Central Connecticut State University, which conducts America’s Most Literate Cities poll, has ranked Seattle as number one or number two every year since the poll started’. He had his own set of challenges in getting Seattle the recognition to join this exclusive club. Having gotten there, It is now among 28 such cities around the world. Iowa City being the only other American location. But those of us who write here know in our bones that this is a city with rare devotion to the written word, says Ryan.

A must do each time I am here and wish to get high is to sit through a book reading or a launch – be it at the Public Library, Athenaeum or the Elliott Bay Book Shop. Ryan quips, The literary effects of our recently legalised cannabis remain to be seen. I have a hunch we’re in for a science-fiction boom. Weed or not, listening to Bill Barry – the NASA Chief Historian’s fascinating account on the space agency’s past and the future plans – I reckon we are already into the realm of fiction. There could not be a better venue for Bill to present than the Charles Simonyi Space Gallery, at the Boeing’s Museum of Flight. Named after the first ever fare paying space tourist. Moreover, the two big boys of Seattle – Bill Gates and Jeff Bezos are significant investors in the business of space exploration. Looks like the critical mass for sci-fi is well in place!

Aqua!

Having covered the sky and the earth, how could one ignore the marine world. The Pacific and the glacial lakes are not only responsible for the sustenance but the dramatic landscape, adventure and the life underneath. The hordes of seafood at the fish market

and the exotic supply for gourmet lovers at all shades of restaurants can spin a mirage. Climate change is hurting and that includes man made interventions.

Tressa Arbow, a budding marine scientist, explains how building dams upstream has been blocking the breeding grounds of salmon. Thereby starving the transient orcas of their staple food. She also explains how PCP dumping in the wetlands, even though banned for a while, is poisoning orcas and killing the calves.

The other night hearing author Kwame Anthony Appiah at the Seattle Public Library talk about his book The Lies That Bind: Rethinking Identity made me think. Rethink about the ongoing philosophical debate on granting human-hood to Cetaceans like whales and dolphins. The human race seems so caught up in its tribal mode that we are all prisoners of identities thrust upon us. Will we and if so when – embrace the super intelligent marine creatures as one of us? Perhaps Seattle will have that opportunity for greatness thrust upon it, too!

The venue was Charles Simonyi Space Gallery at Boeing’s Museum of Flight. The occasion was NASA Chief Historian Bill Barry’s talk about NASA’s impact over the last 60 years, where we’ll be going in the decades ahead, and the six things one probably doesn’t know about the NASA history. Some fascinating questions followed from an audience whose age ranged anything from six months to ninety years.

From metallurgy to life science, earth science, telecommunication, photography, climatology, nutrition – the list of how space research has forever changed the way we live is seemingly incredible. On the competitive side the insights into the space race between the USA and the erstwhile USSR is a fascinating study. How Khrushchev brushed aside JFK’s overtures to partner in jointly putting man on the moon and ultimately how the US finally got the leadership; Lyndon B Johnson’s sustained support to the moon mission post JFK; the age of private sector explorations; the ongoing collaborations at the International Space Station; space colonies; challenges in travelling to the Mars. It was all too riveting.

The traveller into the future…

As Bill narrated how our world has changed dramatically since NASA opened for business on October 1, 1958 and the vision beyond the Moon and Mars – there was another drama unfolding next to where I was seated. Little Russell was merrily learning to walk the terra firma. Blissfully immersed in his pursuit. Falling, getting up, colliding and navigating his way through wherever there was space to be found. He was steadily and determinedly getting ways of the spaceship Earth right!

‘Would you like to travel to the moon and mars’? I asked and he cackled as if answering in affirmative. ‘He might’ said the indulgent mother. ‘He is afraid of nothing’ is certainly a great starting point and an amazing next 60 years of assured action for NASA! Thereby opening fresh frontiers for mankind’s progress and readying to overcome new risks…

Yes, this is all about Ayuthaya – right here in Thailand. About 85 Kms up north of Bangkok! It was the capital of Siam (ancient Thailand) from A.D. 1350-1767. Thirty-three kings of various Siamese dynasties reigned in Ayuthaya, the full name being Phra Nakhon Si Ayuthaya or the sacred city of Ayothaya, until it was conquered and destroyed by the Burmese in 1767. The city was burnt and with it almost all the official records and annals were lost.

Flourishing hub for international trade

From the documents available it appears that the Portugese came to Siam in 1511. The Spaniards in 1594, having gained a foothold in the Philippines in 1565, next came the Dutch in 1607, the English in 1512 and the French in 1662. In those early days, Ayuthaya was a city built upon an island, which was surrounded by several other smaller islands interconnected by a rich pattern of canals or streams. The island on which the city stood was enclosed within a city wall. Inside was the king’s palace and government buildings, and no foreigner was allowed to live therein. All foreigners, whether French, English, Dutch, Portugese, Japanese, Chinese or Indian, who settled in Ayuthaya, lived according to their nationalities, in camps or villages outside the city wall.

De La Loubere, who was a French envoy in Ayuthaya during 1687—88 describes, “The City of Siam is not only an island but is placed in the middle of several islands, which renders the situation thereof very singular. The island wherein it is situated is at present all enclosed within its walls. It has almost the figure of a purse, the mouth of which is to the east and the bottom to the West. The river meets it at the North by several channels, which run into that which environs it, and leaves it on the South, by separating itself again into several streams.

The King’s palace the North of the canal which embraces the city, and by which alone as by an isthmus, people may go out of the city without crossing the river. The city is spacious, considering the circuit of its walls which enclose the whole isle, but scarce the sixth part thereof is inhabited, and that to the southeast only. The rest lies desert where temples only stand.

Tis true that the suburbs, which are possessed by strangers, do considerably increase the number of people. The streets thereof are large and straight, and in some places planted with trees, and paved with bricks laid edgewise. The houses are low and built with wood; at least those belonging to the natives who, for these reasons, are exposed to all the inconveniences of the excessive heat. Most of the streets are watered with straight canals, which have made Siam to be compared to Venice and on which are a great many small bridges of hurdles and some of brick very high and ugly”

Global trade routes

To and from Ayuthaya, there were two trade routes whereby goods could pass to and from foreign countries. One was from Paknam, in the Gulf of Siam, upto the river Menam (now Chao Phya), through Bangkok right upto Ayuthaya. In those days, the river was navigable for sailing ships as far as Ayuthaya, where most of the trade was done. This route was followed by ships sailing to and from China and Japan.

The other route was overland from Ayuthaya to the town of Tennaserim and on to Mergui on the east coast of the Bay of Bengal. The whole trip from Mergui to Ayuthaya or vice versa could be accomplished in ten days. Indian and Peyian traders preferred this route via Mergui to going through the Straits of Malacca and up the Gulf of Siam to Paknam. The Indian and Persian ships did not go all the way to China and Japan, and the Chinese and Japanese did not go direct to India. Siam was the halfway house where these traders met and exchanged their goods. The Chinese & Japanese brought to Ayuthaya silk, tea, porcelain, quicksilver and copper—bronze vessels, and took in exchange scented woods, pepper, hides & birds’ nests.

Along the overland route from the ancient capital to Mergui, dealers lived in Ayuthaya, Tenasserim and Mergui, received from China and Japan goods which were in demand in India and Persia, or vice Japanese articles could be sold in England at a large profit but the Japanese who came to Ayuthaya dealt mainly with the Dutch and the Muslims.

For many years the English East India Company had not considered the Siamese trade as a coast trade and although the Company had maintained agents in Ayuthaya on and off from the beginning of the seventeenth century, these agents had never been able to enter Japan trade. This was due to the opposition of the Dutch who had their headquarters in Java & a fine factory in Ayuthaya, and did their best to keep all other traders, including the Siamese, out of the Japan trade.

The downfall

Interestingly, history of this Ayuthaya too is not free of controversy. According to popular accounts, Ayuthaya met its downfall after four centuries of glory, when it was weakest under someone dubbed as the leper King, the incompetent King Ekadasna. Probably the most detested character in Thai history. During the wars, he reportedly ordered the soldiers not to fire mortars at the Burmese troops because his concubines were frightened of the noise. And he eventually met his pitiful fate by dying from hunger during his hiding!

While history has made Ekadasna a bad guy, the Thai historians are questioning whether he was really incompetent or was he a scapegoat? Was Ayuthaya really militarily weak at that time? Were the Burmese troops mere guerrillas, not a fully supported army? An alternate school of thought seems to be emerging.

Today the ruins are but parts of a boisterous town. Booming largely on the account of upcoming industries in the neighbourhood. Tourism of course accounts for a sizable revenue. It takes an hour and half from Bangkok to drive down the excellent highway heading to Chiangmai, further up. There are regular luxury buses plying to and fro Ayuthaya.

Seats could be booked for a keen tourist by any hotel. Another alternative is a one-way cruise onboard ‘Ayuthaya Princess’ on the Chaophraya river. The package involves a return by airconditioned buses.

This time it wasn’t the Chanakya Cinema, New Delhi, that peak monsoon morning seventeen years ago. Where I sat drenched, in the front row. Having arrived after a marathon city bus ride from the Delhi University campus. The show btw cost me a mere sixty-five paise.

Yes, to be in time for The Bridge on the River Kwai. As the brilliant action unfolded, the extra efficient air-conditioning and the close proximity to the seventy mm version of this World War Il act, elicited all the willpower I could muster. Afterall I could not belittle myself witnessing the heroic deeds.

Tonight too I was in the very front row, but of prime seats at a sound and light show. Right on the water front of river Khwae (Thai for Kwai). Having driven 140 Kms from Bangkok to Kanchanaburi, close to the Burmese border.

Historic Kanchanaburi

Kanchanaburi is a small sleepy town abuzz with tourist activity. Having landed there during the mid-day, one started with the war memorial. It houses fifteen thousand graves of the allied soldiers. Laid neatly in the green backdrop and rose beds. One of the walls at the entrance bears testimony to the heroic deeds of the Indian soldiers. Its caption reads “These soldiers died serving their country and the cause of freedom and lie buried – elsewhere in Thailand”. They represent the various units of the Indian Armed Forces viz; The Corps of Royal Indian Engineers; Q.V. O. Madras Sappers and Miners; 13th Frontier Force Rifles; 14th Punjab Regiment; Indian Army Medical Corps; Indian Army Veterinary Corps; Indian Army Ordnance Corps and Indian Pioneer Corps.

A quick lunch at any of the several eateries and you could be back on your feet. The JEATH War Museum is not an absolute must. But if you are in Kanchanaburi during the River Kwai Festival Season, as I was, the entire place is like a big flea market. Wares ranging from woollens, to Chinese cigarette lighters, handicrafts and local jewelry are abundantly available. All for a bargain. Also on display at the official jewelry and gems exhibition is the country’s biggest 40 carats blue sapphire. Mined from the Bo Ploi District of Kanchanaburi province.

The eleven day festival which has now become an annual feature, (last week of November to the first week of December) commences with a Don Rak Thai religious ceremony conducted by dozens of Buddhist monks. It is followed by a Colourful Peace and Love Among Humans procession from the City Pillar Shrine to the Bridge. The 240 hours of festivities include special attractions such as traditional long boat races under the bridge, a mini marathon and a Miss Peace Thailand Beauty Contest.

Just as the dusk takes you by surprise, thousands of lights transform the bridge, river and the surroundings into a fairyland. The restaurants along the river front start filling up. There is also a scramble for getting the right seats for the show. The cool breeze takes many a visitor by surprise. Sale of windcheaters and sweaters warms up. There is an air of expectation.

Simulating the war theatre

The sound and light show commemorates Allied bombing campaign that neutralised the infamous 415 Kms of Death Railway from Ban Pong to Thanbyuzyat in Burma during World War Il by Allied POWs . Working to the brutal Japanese chant of “speedo”. Commenced in October 1942 from both the Burma and Thai ends, the rails were joined at Konkuita wartime camp, some 37 Kms south of Three Pagoda Pass in October 1943. It is supposed to have cost lives of 16000 POWs and 100,000 Asian labour. Interestingly, today it is an enormous Japanese investment that has reportedly helped develop the provinces’ infrastructure.

The show commences dot on time. A train rambles across the bridge. An occasionally sharp whistle perhaps helps it to pierce through the artificial mist on the tracks. Chuck, chuck, chuck… And suddenly there is a commentary (in ‘phasa’ Thai). If you plug in the earphone you could hear the English version. But it is the sound effect that leaves you completely overawed. In no time you are in midst of a war theatre. The Japanese brutalities, cries of the POWs – all seem too real. Just when it begins to feel unbearable the aerial attack commences and so do the ack-ack guns, the sirens and the activities of the Red Cross.

Large amount of dynamite and other deafening explosives recreate the Allied bombing on the bridge. Explosive charges floating in the river are ignited to send huge columns of water spouting up into the air to imitate a near miss by a 2K pound bomb. The destruction of the bridge is quite spellbinding. It virtually creaks and ‘drops down’ into the river. Incredible, particularly for those who have strolled across it during broad daylight.

There is a feeling of shell shock as well as relief, as you emerge out of the show. And if you choose to drive back to Bangkok the same evening – as I did – the dramatic experience will surely keep you wide awake all through the next two and a half hours!

It was the summer of 1995. I was in Taipei, face to face with my local accomplice Tom’s friend. We exchanged our name cards and had a handshake. As if anticipating the query, he said “Yes, I am Gandih King”.

“What a remarkable name”, I said.

“It is the same as Gandhi”, said Gandih.

It was not turning out to be very helpful!

But he soon came to my rescue. In the process I had some glimpses into the story of his life. The family had escaped the uprisings in China and landed in Calcutta – his birthplace. Soon after he was born, he said his father heard about Mahatma Gandhi’s assassination on the radio. Thus the name. The father spelt him the way he spoke it!

Having come this far, I ventured a little further.

“What about the other half of your name”? Before I could draw any other plausible conclusion he interjected ” That’s my real family name”. After all he did have a swadeshi component.

I was barely recovering when the driver of the cab we had gotten into got involved into an animated discussion with Tom. It is nothing unusual in Taipei. What is unusual is how they simultaneously navigate the dug up roads readying for the upcoming underground, also smoke without your permission and effortlessly glide over a random earthquake tremor. But quite unlike Singapore or even Ho Chi Minh City – they know no English here.

“I just replied to the cabbie that you are an Indian”, confirmed Tom. However, I suspected that the conversation was actually a little more elaborate.

And then, “Why are there so many crows near your airport?” was a bit of a googly for Tom who had never visited India.

“What does he mean – has he been somewhere in India?”, this was my turn to ask.

Some dialogue and then followed the interpretation, “He cannot remember which city it was. Yes, he has gone to your country many many years back when he was a sailor.”

While he drove and yapped, boy he would swerve from one lane to the other. Even try eye contact with both of us through the rear view.

” Please tell him he drives just like a sailor”, I said to Tom.

He took that as a compliment. And broke into a wild laughter.

” I like the Indian style driving – very exciting”, he conveyed. Perhaps as a return compliment. He insisted on shaking hands as we parted. Some vigorous shake that was.

There was more yet to come.

That evening some friends invited me over a cocktail organised by an Indian Association of sorts.

They were felicitating the head of the newly set up Indian Trade office in Taiwan. I thought it would be a good opportunity to meet a lot of people at one place.

So I found myself mingling into a big crowd. Exchanging courtesies. Just then “I am Vinod Khanna”, said this Bollywood namesake. A retired diplomat. The suave gentleman was the one taking over as the head of the trade office.

The name was bound to evince a lot of curiosity. And it did.

I cannot conclude without telling you what Tom narrated happened to him in New York, where he was on a one year study leave. Tom is a Taiwanese business associate and gets along very well with the small Indian trading community in Taipei.

“One day I bought a newspaper from an Indian hawker in New York who wouldn’t accept any money. Then he says “Tom, don’t you remember me? You used to visit our office in Taipei.” For Tom Ko this was the strangest thing that had ever happened.

Strangely enough, for me it was an overdose of Made in India stuff. Made in Taiwan!!!

It is always fun enhancing and embellishing a presentation till the very last minute! It can get a bit stressful though. So, there is never a final ‘final’ script. Onboard an Air China flight to Beijing recently, I spot this feature in the China Daily. Gamers: New era dawns for China in e-Sports arena. It fits so well into an exploration on who is your customer – a part of my presentation to be.

- According to the League of Legends Pro League, live broadcasts of its games were viewed more than 7 billion times by Chinese fans in the first half of this year.

- By 2020, the market value of e-sports is expected to exceed 20 billion yuan. Last year, there were 250 million Chinese gamers which is expected to go up to 300 million by 2020.

- North America and China are the two major pillars of the global e-sports industry, accounting for 37 percent and 15 percent of the market respectively.

Watch-out the yo-yoing of the potential customer:

Will the PlayStation and Xbox generation age into a very different profile as they metamorphose via the e-Sports? Mind you, we are looking at very large numbers of Gen Y and Z. How will these impact the ‘real’ sports? As they enter the mainstream would the traditional sports be marginalized? e-Sports seems all set to enter the Olympics! Last but not the least, will any such engagement not only delay the behavioral ageing of digital natives but also witness a reversal in the lifestyle of ‘oldies’ who get hooked on to e-sports at some stage of their life?!

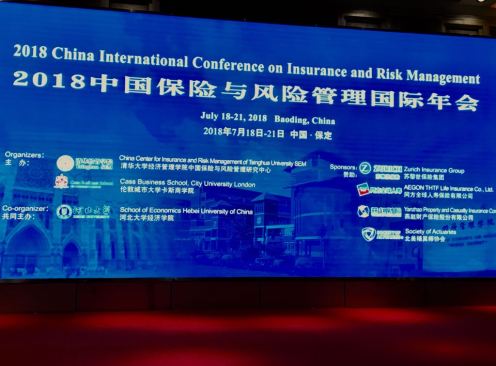

Once at the venue hotel in Baoding, Hebei (literally north of the river – Yellow river: cradle of Chinese civilization going back to 4000 BC) to attend the China International Conference on Insurance and Risk Management (CICIRM 2018), I am just in time for the inaugural dinner. No sooner I exchange greetings with the gracious host Dr Bingzheng Chen of Tsinghua University, his first question is what brings me to the CICIRM year after year. Starting with Kunming, Shenzhen, Hangzhou, Xian, Guilin (could not present in person) and now Baoding!

Three things, I tell him. First, volunteering into an ‘uncomfort zone’ – constant each time. Second, refine understanding on the subject of my presentation this year: “The Cyber March of Human Civilization Puts Insurers at Cross-Roads: Potential Threats & Opportunities!” Third, is to meet the ‘Buddha of Insurance’. He is certainly not one who fishes for compliments. My reverence stems from his dedication to drive change by lifting the intellectual bar of the industry-academia partnership and applying it with full intensity at the grass root levels of the societal needs. One look at any of his event agenda will tell you what I mean.

Dr Chen ushers me to an English speaking table and I end up in the most fascinating company of an Israeli couple from Haifa and a group of Professors from Mongolia. The first being a charmed pair of silk route explorers and the other literally at the heart of where it all originated. However, both at two sides of the digital silk route divide.

‘It’s not the economics, stupid!’

The keynote address from Professor David Blake, Professor of Finance and Director Pensions Institute, Cass Business School – the following morning, is a wakeup call and sends me scurrying to ensure that my presentation for the next day factors this new onslaught. David graphically demonstrates how It’s the demographics, stupid! at the very root of stagnating productivity in the developed world.

- Longevity risk: Systematically underestimated 1840 onwards, life expectancy has gone up by 2.5 years per decade.

- Rise in life expectancy + decline in fertility = Ageing.

- Politics of underestimating life expectancy: Thereby passing on taxes to the next generation.

- A third of babies born in UK will live 100 years and retire at 60!

- Japan already the oldest; Korea will be second oldest; UK 20 years behind Japan; US witnessing the beginning of the population problem. China: Lucky and unlucky generation – effects of public policy. From an ideal situation where more young people would support less old ones, lesser and lesser younger ones supporting more and more ageing. Thus the Inversing Pyramid!

- Consequences of an ageing population: Automation; gig economy; products and services for the elderly ; one third of the jobs in developed world by robots; New tech versus the previous.

David cites a shocking case of a nonagenarian mother shooting dead her septuagenarian son who insisted on shifting her to an old age home! Suddenly, my profiling of the customer becomes convulsive! E-sports can be fun but David shuffled the tectonics rather vigorously. After him came Shaun Wang from Nanyang Singapore and he talks about disappearance of ATMs and enunciates his ‘peeling of onion’ theory – thereby unsettling my thoughts even further. I am transposed somewhere between Brave New World and Future Shock. Also wondering as to how Asimov might wish to adapt his Three Laws of Robotics to fit this situation?

The Discussant:

Frankly speaking, I was not aware of any such role till my first ever CICIRM experience! All presentations ought to follow a brief commentary by a discussant. And as a presenter you also end up being a discussant for someone else. Ze Chen, a bright young PhD student from Tsinghua turned out to be mine. What do I learn from him, with regard to my presentation, going forward?

- Provide more background for the audience: e.g. insurance 1.0, digital insurance 2.0.

- More detail about the survivor kit: Actions if insurers are to compete.

- To be more specific with one or two illustrations, e.g. How Insurtech works as a solution?

Points well taken! My theme shall encompass these aspects in future, Chen San…

Guanxi:

The restaurant on the 18th floor has a Peking University logo and reads Baoding 1898 Coffee. As I find out later, it was set up by someone who once studied at the same University. Here I am in the company of Frank, Jino and Joy my new found network of very smart young global Chinese. All a product of the one child policy generation and delegates at the event. Frank is the only one with with an older sister and lucky to have gotten away given his rural origin. We confer sipping the iconic Arctic Ocean yellow soda which has a huge following in north China. One of the several successful local brands with global scale but unknown to the rest of the world.

Coffee. As I find out later, it was set up by someone who once studied at the same University. Here I am in the company of Frank, Jino and Joy my new found network of very smart young global Chinese. All a product of the one child policy generation and delegates at the event. Frank is the only one with with an older sister and lucky to have gotten away given his rural origin. We confer sipping the iconic Arctic Ocean yellow soda which has a huge following in north China. One of the several successful local brands with global scale but unknown to the rest of the world.

Baoding with a population of 10 million, I hear from my guanxi, is an outcome of the government’s attempt to decongest Beijing and move away the industry. From the window, against a setting sun, one can see the frenetic pace at which the city is under construction. I also hear them tell me how the younger a mayor taller are the buildings in his territory and about the upcoming five star jails! I am pleasantly surprised and swamped by their fascination for the IITs; it’s alumni who make some of the best Professors in the US; questions on family traditions and marriages. Including whether they could seek an admission at the IIMs? Here was, I thought, a breed which had transcended the colour of their passport – intense curiosity, hungry to grow and seek best in class stimulation wherever it could be found… At the end of the meal Frank volunteers to settle the bill. Within seconds the rest pay back their share via the hugely dependable WeChat!

Dr. Imelda Powers, a PhD from Yale, is a global authority on CAT Modeling. Her husband Dr Michael Powers, a PhD in Mathematics from Harvard, is a Co-Chair at Tsinghua SEM with Dr. Chen. Following her insightful presentation I am very keen to hear her thoughts on modeling Cyber risks. My follow-on question would have been relating to lifestyles of the digital natives and resultant aggregates. Imelda reminds us that both liability and cyber classes are still in the baby stage of evolution! ‘Give them some time’, that we need more data and experience is what she alludes to.

Beating the retreat:

I decide to take a shuttle bus instead of the bullet train on my way back to Beijing. The three plus hour drive would give me enough time to build upon my exploration of last few days basis what I have imbibed. It turns out to be super smooth and visually very pleasant with both sides of the highway lined with thick green foliage.

On my rear seat is this playful child in company of his doting grandma. What impresses me is the strong bond between the two. As we advance towards the destination, traffic slows down and little Tim’s (that’s what I believe I heard) temper gets nastier. Maybe he is hungry, sleepy, bored – a child after all. It is then that a lady occupant each – on the seats ahead – give little Tim a mouthful. Silence returns. So, the young lady two seats in front turns out to be the mom, behind her is her mother. The boy is actually in the care of his great grandmother!

Going back to David Blake’s hypothesis – Tim could sooner or later end up supporting all three women! A reverse pyramid seems more daunting than the Great Wall! In his blissful slumber, Tim is back to his angelic self. Perhaps e-Sports would be his moment of relief when grown up and whenever fully awake?! He could very well fuel China’s glory at the FIFAeWorldCup. Laced with some new perspectives and dimensions, I thought the presentation was future ready – for now!

July 2018

Wimbledon in a year of the World Cup Football cannot be just tennis alone! Moreover, hopping on and hopping off black cabs, private taxis and the Uber gives London yet another dimension.

The shortest ever answer to the immigration officer’s ‘what brings you to London?’ – Wimbledon – is like a magic password. At the Earl’s Gate station, nearest to my stay, the staff doesn’t need to second guess as to where one is headed. ‘Remember to get off at Southfields and follow the crowd’ is all you are told.

At this moment all the dominant football chatter, in whatever tongue, onboard the Heathrow Express – recedes. The cabbie’s reaction to mine ‘whether Uber still exists in London, given the ongoing controversy’ was nothing surprising and set aside for further validation!

Suddenly, I become conscious of my pilgrim status. What must be an otherwise sleepy station, now has a concentration of fans from the world over – headed to the Mecca of tennis. A Grigor Dimitrov for Hagen Dazs ad beckons you to a strawberry and cream treat. Part of the platform is covered with a green mat suggestive of what awaits ahead.

Once out in the open at the Southfields, the option is to keep walking in the direction of SW 19 or take a cab-ride for ‘just two pounds to tennis’. Most prefer to march the picturesque downhill. Intense conversations can be heard on anything ranging from previous years to previous days, today and the beyond! Some stop by to reinforce their headgear or any other form of bargain, food and drinks that spring up between beautiful homes with pretty gardens. There is even a Maui Jim outlet. Many who you do see wear a straw hat inside the Club – probably picked it here. Every step is an exciting buildup to the drama that is about to unfold.

On my day 1 commute, I am focused on the first match at the Court 1. In my mind it could be a Halep versus Kerber clash at some advanced stage with a good likelihood of one of these coming on the top. There is no doubt whatsoever that today Halep should be able to overcome Hsieh. A quick strawberry and cream treat at the Food Court and I am one of the first one to get inside. Much before even the net comes up. It is amazing to be inside that arena awaiting the arrival of the spectators and the gladiators. Am I overwhelmed? That would be an understatement!

Much to everyone’s surprise the slightly built Taiwanese girl not only matched Halep’s screams but outplayed her in every department. Game after game one expected the recent French Open champ to pull something from her armour to neutralise the challenge. But that was not to happen. Perhaps this was an exception?! Falling seeds seemed to be the underlying theme all throughout. Nothing could be taken for granted. The day after this heady win Su-wei too fell – to opposition – at one of the side courts.

Later in the day the Gulbis and Zverev match saw the departure of the high seeded German whose temper in parts dominated his talent. And in the last of the contests Nishikori outwitted Kyrgios, thereby challenging the very rationale of seeding. The same day while Russia and Croatia were also clashing, it was Sweden versus England that registered its presence in the thick of the tennis drama. None should have missed the passionate ‘come on England’ call at the Court 1.

My day 2 at the Court 1 started with a Kerber versus Bencic. A spirited one but the German girl prevailed over the Swiss Miss. It was in his match with Monfils that one saw the raw power and surgical precision of the ‘skyscraper’ Kevin Anderson. This followed Djokovic annihilating Khachanov. The Serb looked too good to be written off too soon despite all the media speculation.

The France and Belgium match was expected to be an epic not worth missing. For many locals the discussion was around who might they possibly play in the finals if they overcame Croatia.

I woke up on my day 3 with a most incredible text informing me about the Federer play on Court 1. Had to literally rub my eyes a couple of times to make sure it was not a dream. ‘Fans who probably bought the Court 1 seats months ago, had no idea they would be seeing Roger Federer’, commented Patrick McEnroe. Likewise, after winning the first two sets, the Federer loss to Kevin was a bit too surreal. Just when I thought the match was getting one-sided, the tide turned in the favour of Anderson. The Court became near empty soon thereafter. Some who had the option of moving to the Nadal match at the Centre court did that while many rushed to follow football.

The prospects of watching Federer play from a close distance was an absolute treat and a dream come true. But then what a rude awakening! Howsoever disappointed I was with the untimely Roger exit, I decided to stay put and watch the two big North American boys – Raonic play the giant Isner. The after effect of the first quarter final of the day was telling. And I even contemplated the possibility of getting some AI into the tennis racket… If only Roger had that luxury, he would not have squandered some of his backhands into the net! Some wishful thinking, isn’t it?

With a cool breeze, after three warm and sunny days, came the news of England scoring a quick first goal. However, by the end of it all just as the faithful headed back for the return ride to Southfields, the mood was somber. Some like me were still reconciling to the GOAT’s demise from the championship and the others smarting from the three lions’ loss to Croatia.

We all love the re-emergence of Novak Djokovic and salute the marathon man Kevin Anderson. That despite the comeback, Novak is not yet in the top 10 speaks for why not to take the business of seeding seriously. And with a roof in place on the Court 1 (come September) there will hopefully be no need to obsess about the bees in your bonnet (alluding to the bee attack on Court 1 ahead of my time)! But could that ensure a zero distraction to the champions from the likes of fluttering butterflies (Roger and Rafael) and the noisy jet engines (Roger) – flying to and fro?

PS: Now all about the drivers!

- Never got to know the name of the driver (black cab) who drove me from Paddington. When asked about the existence of Uber. The response was rather curt. ‘Yes they are very much here. As always upto their usual tricks!’

- Abdul (private cab) Afghan origin. Drove me from Earl’s Gate to Pall Mall. Came in as a refugee when he could still learn to drive in London with the only language he knew then – Pashto. His first employer was a Gujarati. Hence more keen to talk in both Hindi and Gujarati. Was invited by the employer to attend the son’s ‘lagan’ in India. Could not make it due to his visa status then. But anyway got to know ‘lagan’ means marriage! ‘What brings you here’, he asks? ‘Oh Wimbledon, I dropped a guest there the other day.’

- Sattar (private cab) Iranian descent (native of Bandar Abbas) and could speak Hindi thanks to his burqa trading days in Dubai. His ‘cutter’ was from Mangalore not Bangalore (he mentioned twice). Very happy like Abdul for having made UK his home. Drove me back to the Heathrow Express. Exceptionally warm human.

- Nuno (Uber) originally from Portugal. Drove me from Trafalgar to St Pancras. Very critical about his home team. ‘There is only one real player. The rest keep looking at him’! His most preferred team lifted the Cup. On private cabbies: Always spreading rumors…

- Ilchan (Uber) a Turk from Greece. Drove me from King’s Cross to Aldermanbury. Cool guy. Happy bachelor. No more girl friends coz ‘they call you all the time to know where are you’! Takes a break when he thinks he has had enough. ‘Who knows, I might get married one day’! What about the other cabs? ‘They are only available in limited places and not round the clock. We are available all over, anytime’.

Between running two Tech events popped many a question (and some answers). Bangalore was about exploring “New World Governance & Risk Order: Responding to Technology Disruptors!” Srikar Reddy, the keynote speaker, reminded of the compelling pull of the internet. As a result, everyone commenced parking everything on the World Wide Web. And then, suddenly we began witnessing the enactment of the ancient silk route! The free flow of global commerce started getting disrupted by the robbers and warlords. As a result one of the biggest businesses as on date, alluded Srikar, is about securing digital assets. There comes in Cyber Insurance, which literally continues to grope in the dark as of now.

Ahead of the announcement of Trump-Kim summit in Singapore just before the second event – this time a two day forum on Cyber Insurance in the Lion City – pilgrims at the Berkshire Hathaway AGM heard the ‘Oracle of Omaha’ pronounce his verdict. That there’s a 2% chance of a $400 billion cyber-based disaster happening each year!

How do we deal with many a Future Shock of a Brave New World?

Not too long ago I recall quizzing a group of young health actuaries as to how would they look at humans living up to 300 years. While today this is scientifically possible, it just did not fit into their logic. Some suspected I was alluding to science fiction! But if only we took Sci-Fi more seriously – we would be readier to deal with the woes that the cyber world has brought upon us. Asimov’s “Three Laws of Robotics” have been around for 75 plus years and Ray Kurzweil continues to amaze with the future of inventions and discoveries.

Popular literature and even bestsellers can put readers into a sleep easy mode. I pulled out from my collection a book review going back 22 years. Cybercorp was a great read on how the author foresaw the future of corporations enabled by the internet. Those were the heady days of this new found magic mantra, just as blockchain is today. But then the review was dismissive of hacking. While answers to the poser from the Oracle must be found and will be found – one ought to proceed with caution. The journey from known unknown to known known must be undertaken.

Anyone can find the answers provided you are future ready!

And that is the tough one. It is not really about your education or background but the mindset. Insurance is a horizontal business. It ought to relate well with all aspects of life in general. Yet we choose to prefer staying in silos. Insurers settle huge amount and number of claims yet the trust quotient remains weak. We believe digital is indeed the solution to this crisis even though premium and claims optimisation may be staring us in the face. Buying stakes in InsurTech is not going to make a disruptor out of an incumbent. The biggest risk to insurers from the world of cyber is fundamentally very existential.

All my panelists at Bangalore (and a few in the audience too – who threw up some profound thoughts on the likes of wave theory and the future of workforce) were future ready because they understood technology, its working and ramifications. None was an insurer. One of them, a US qualified attorney practicing out of the UK, shared some amazing insights into her current work. All the cases handled are analysed by artificial intelligence – all she does is be a friend and adviser to the clients.

At Singapore all but one speaker (an Ivy League educated techie) were from the mainstream insurance and only one speaker from the industry had a tech background. The general trend today is cyber as a part of financial lines & casualty underwriting. That does break the silo. Yet, despite the ‘horizontalising’ effect of cyber, many tend to allude to systemic risks and cross-class covers. That to me is an oxy-moron. So, from all those who stayed back for the concluding session on the day two, I sought some out-of-the-box assistance:

- A marriage in Singapore was annulled because the husband decided to become a female. The local laws prohibit same sex marriage: What could possibly happen to various forms of insurance coverages?

- A transgender male in Finland becomes pregnant: Implications for insurance contracts?

- If humans do begin to live up to 300 years and in due course metamorphose from a pure human to a cyborg: How would underwriters evaluate and cover such a risk? (Needless to mention Michihito Matsuda the robot who garnered third highest votes in Tama city mayoral elections, Japan).

The first two being very recent facts and the third still fiction – are of real interest to me also as a student of diversity. And not surprisingly enough the process left a few in the cohort rattled!

What must insurers do to get closer to the ‘known known’?

Perhaps raise the bar and align their vision to something very compelling. I found one in this quote from Jeff Bezos. “Now take the scenario, where you move out into the Solar System. The Solar System can easily support a trillion humans. And if we had a trillion humans, we would have a thousand Einsteins and a thousand Mozarts and unlimited resources and solar power unlimited for all practical purposes. That’s the world I want my great-grandchildren’s great grandchildren to live in.”

Cyber is certainly an opportunity for insurers to be future ready. The first step in the journey towards arriving at the known known is after all the resolve to deal with the unknown! Let us, therefore, not lock up cyber insurance in a silo but rather tap into its power to unravel the unknown for us…

A painting (photo) by Rai Venkatchallam, in the collection of the Salar Jung Museum, that shows Mah Laqa Bai’s extraordinary presence – the only female in a landscape of men. She can be seen in her palanquin at the upper right of the painting.

Ratika Sant Keswani (RSK) is an accomplished stage artist. Her exquisite enactment of Mah Laqa Bai or Chanda Bibi (1768-1824), a product of the eighteenth century Deccan, gives her a unique opportunity to explore the remarkable personality. The Q&A brings out Ratika’s passion for diversity and highlights her empathy for this versatile and defiant historical character.

For the last twelve years Ratika has been part of the financial services. She currently works for KPMG, based out of Hyderabad.

PG: Your insights into her and her upbringing?

RSK: Mah Laqa was in the truest sense “woman of substance”. She not only was a poetess, but a courtesan, a philanthropist, a warrior, an exceptional swordsman, a very important and trusted member of the court of the Nizam for the state policy matters and was appointed as Omrah (senior nobility).

Born in 1768 to Nawab Basalat Khan Bhadur and Raj Kuwar, she was given away to her older sister Mehtaab Bibi, who was unable to conceive. Mehtaab Bibi was married to Rukn-ud-Daula, the 10th prime minister of the Nizam. Horse riding, languages (Urdu and Persian), poetry, sword fighting were her favourite subjects. Once she showed interest in poetry and music she was taught and mentored by the greats of the time. She was trained in classical music by Kushal Khan Kalawant – great grandson of Tansen, a master musician. She was a pious woman, a devoted mystic, greatly influenced by the Sufi and Bhakti elements.

She probably entered the court of Nizam as a courtesan but rose to the level of senior Omrah (highest nobility) basis her intelligence and wisdom.

PG: Challenges she faced?

RSK: To survive & excel in man’s world!

To be a warrior – she fought 3 wars, dressed as a man. She was an expert swords-woman & archer.

To be accepted in the court of the nizam as a policy advisor.

To excel in her area of interest – poetry, and participate in mushairas, those were restricted to men.

To move beyond the labelling of a “courtesan”.

To be okay being a courtesan so as to enjoy the perks of freedom and out of bounds of any male control.

To remain unmarried, and adopting young girls to give them a quality life and future.

Moving on in life knowing that the love of her life used her love, loyalty and devotion for his personal gain.

PG: How did she break out of the glass ceiling of her times?

RSK: By being Fearless. She used her intelligence and was persistent to achieve her dreams.

PG: What did she choose to write on?

RSK: Her poetry is a reflection of her own experiences at the time. While like most, her ghazals are also about eternal love, faithfulness, pain of abandonment but one can also see references of the state politics through enmity, fidelity, intrigue and her mystical devotion to Hazrat Ali – the saint.

PG: If she were to reborn today, what could be the challenges that she might face?

RSK: To excel in a man’s world!

Challenges are the same – just that now survival is easier for women, the bigger problem is that women want to excel more than ever. So they have to constantly fight – fight stereotypes, fight inequality, fight to balance work & family, fight biases of what she can and cannot do, fight to lead and not trail.

PG: Many thanks & best wishes in all your endeavours!

Home » Knowledge » Blogs » Predictions for 2018

Predictions for 2018

Published Date: 05 February 2018

Last Updated: 05 February 2018

Praveen Gupta, Chartered Insurer, looks forward to this year’s expected trends

First, a confession: I have no crystal ball to gaze into! What I am relying on is a combination of wishful thinking, past scribblings and current trends.

Overall, 2017 was a year of turbulence – mind, matter and nature were all put to extreme test. And 2018 may be no different – it will surely help if we resolve to think differently. A product of the industrial age, insurers must reconcile with the fact they are now deep into the information revolution. The playing field, and therefore the rules of the game, have changed.

Here are no projections or numbers. No linearity of thought. These are just a handful of defining and definitive tectonic shifts:

- Insurers (and reinsurers) coming of age? While these are early days of ‘going cold’ on, say, the coal industry, insurers seem to be getting ahead of banks. But this is not about insurers versus banks. With the US backing out of the Paris Protocol, could industry groups wrest the influence from the state? I believe insurers should begin influencing the direction of debate on climate change. The recent decision from a few insurers to pull out of coal is only the beginning of a long saga. The fossil fuel industry will be under increasing pressure. Insurers will surely have an opportunity to ensure the centre of gravity moves in their direction, as non-state players take on the role of influencers.

- How green is my policy? The ‘E’ and ‘S’ components in ESG, rather than just the quarterly performance, will drive the stock price and overall governance. Investments in the likes of the tobacco industry, and revenue and profits from fossil fuel, will increasingly turn off investors and stakeholders. Trust will be a function of reputation. Policyholders, customers, investors and other stakeholders will be very mindful of an insurer’s reputation. Boards will be required to spend more quality time on ESG. Diversity in thought and practice, and converging action by roping in talented external experts, would make the insurance industry more meritocratic. We saw Sian Fisher taking a lead for financial services on the ‘HeForShe’ campaign – expect more of these. A superior ESG play will be a booster for our industry.

- Cyber or what? A chief digital officer (CDO) rather than a CMO or a CFO is more likely to get into the corner office. Why? Thanks to being a common denominator, it will facilitate cross-class covers bridging the full spectrum from tangible to non-tangible, product to solutions, centred around discontinuity and reputation. It will also ensure efficiency and transparency of asset allocation in risk transfer mechanisms. This ‘flattening’, courtesy of cyber, will also begin to result in the early days of pushback against the protectionism that is in-built in the form of admitted/non-admitted coverage. This will eventual lead to the removal of political barriers.

- Signals or noise? Let’s not forget that there are too many of these confusing the customer. While the signals bode well for customer journeys, the IOT, big data, AI, blockchain, et al will continue causing excessive noise. This calls for a lot of hand-holding in this transition. Insurers will need to ensure they optimise on trust while they struggle – regulators will begin to blow whistles on account of price and claims optimisation! This year will surely tell us whether there is more space for the likes of Lemonade to grow, whether there will be more Lemonades, or perhaps only Lemonades beyond 2018!

Praveen Gupta is MD & CEO at Raheja QBE General Insurance Co