Our oceans are the most critical climate regulator. Humanity cannot survive without a healthy marine ecosystem,” says marine biologist Dr Howard Dryden. “We could survive climate change; we will not survive the loss of marine life and the ocean drifters that life on Earth depends on,” he warns.

Wally Daudrichis a Churchill based eco-tourism entrepreneur. He runs Lazy Bear Expeditions and captains Matonabee. Located in the far-flung northern end of central Canada – by the Hudson Bay – Churchill is a small town (population of approximately 800) in province of Manitoba. Best known as the polar bear capital of the world.

Praveen Gupta: How did Churchill evolve from a military base to an eco-tourism destination? Please describe your early venture in eco-tourism.

Wally Daudrich: The military represented a boom for an otherwise small coastal village. The boom ended when political and scientific conditions changed and there was no longer a need for an early dispatch airport for countermeasures to Soviet threats. Those threats dissipated with the development of satellite warning systems.

Ecotourism in the world didn’t start to fully develop until a consciousness of our environment that we live in needs to be balanced with sustainable economic development.

Churchill was a fur trading village for centuries. It was unique in many ways as it developed a trading system that benefitted both Indigenous people and Europeans of that day.

“During the military days there was very little activity of bears coming into populated areas… When the military left the bears moved in.

At first the polar bear was viewed as a nuisance. During the military days there was very little activity of bears coming into populated areas. By virtue of the amount of activity, the Polar Bears generally stayed away. When the military left the bears moved in.

As this made news of actual polar bears walking through Churchill it generated millions of dollars of free publicity before the internet and social media became the main comms method. Local businesses grew around the demand for local polar bear tours near Churchill.

When the sea-ice melts, polar bears wander in and around Churchill!(Picture by Amiya Gupta).

PG: The Churchill ecosystem is at the intersection of three biomes and show-cases large polar bear and beluga whale populations. What are the unique circumstances that arise at this intersection?

WD: There are several natural forces that create the apex mammal life in Churchill.

First, the proximity of Churchill near four river systems helps to create a brackish water environment. This attracts fish and spawning concentrations in the area. And of course the concentration of fish brings the high fat concentrated mammals of seals and whales. And as a result the apex predator is here in higher than normal numbers.

“The concentration of fish brings the high fat concentrated mammals of seals and whales. And as a result the apex predator is here in higher than normal numbers.

Also, geographically we have a large peninsula called Cape Churchill. This peninsula in conjunction with the ice spewed out by all the river systems helps to cause the area to freeze up to 2 months sooner than other parts of Hudson Bay.

Polar bear holding place! (Picture by Praveen Gupta).

The proximity of the Boreal Forest and the Tundra biomes are largely irrelevant to the success of the polar bears in this area. But they are interesting in how the species interact from the different biomes.

PG: You have been observing the Churchill environment for 45 years, how has it changed with global warming and how will it continue to change?

WD: I believe that in general the climate is warming. But I believe it has been warming as a general trend for thousands of years. Polar Bears will not start to die like we sometimes see illustrated by organizations looking for donations. They slow down reproduction.

I have seen our local population fluctuate over the almost 5 decades as we see volcanoes, and other natural events affect the temperature of our summers. The overall changes I see are not alarming me. I also see a number of behaviour adaptions from the bears which allow them to hunt successfully each summer.

“Polar Bears will not start to die like we sometimes see illustrated by organizations looking for donations. They slow down reproduction. I have seen our local population fluctuate over the almost 5 decades.

PG:How can eco-tourism help reinforce Churchill’s biodiversity?

WD: Ecotourism in Churchill is terribly political. But the rewards for those who work hard and provide honest service and integrity will pay off albeit sometimes with years of adversity. I have seen it myself as I grew my business that the eventual jealousy’s flare with our competition.

Spot the ‘white fluffy thing’ from the water front – onboard Matonabee – in the good hands of Captain Wally!(Picture by Praveen Gupta).

PG:What can budding eco-tourism destinations learn from the Churchill story?

WD: Make sure that there is opportunity for younger generations to create their business and thrive. Regulations are good. But there has to be a balance of freedom and regulations to keep innovators in business.

PG: Can you please expand on the interaction of species such as red fox and prairie fox / and the whales in this eco-system (belugas, bar heads and narwhals).

WD: Conceivably red fox and Arctic fox are close enough that they can actually breed together. Although I’ve never seen. They typically are at war with each other. The Arctic fox is significantly bigger and more robust than the red Fox of southern Manitoba. As I mentioned to you – our red Fox have various colour schemes that are normally not seen anywhere else. The Arctic fox are quite prolific breeders. Sometimes having as many as 24 young.

Arctic fox have been able to adapt to an Arctic coastal environment and often will follow the polar bears out on the ice to scavenge after a seal kill. Red Fox will not. Red Fox feel more comfortable in the boreal forest surrounded by trees and willows.

“Arctic fox have been able to adapt to an Arctic coastal environment and often will follow the polar bears out on the ice to scavenge after a seal kill. Red Fox will not.

Much of what surrounds Churchill is actually not tundra, but would be considered Tiaga – a Russian word which means transition. The transition between the boreal forest and the tundra. The word is noteworthy because the true Tiaga transition area near Churchill is about 100 miles wide and makes a significant geographical area.

Or be driven – for bear spotting on a tundra buggy – by a brilliant guide & story-teller Rob Watson! (Picture by Praveen Gupta).

Once you get north of the tree line onto the tundra the food supplies is significantly less for animals like the Arctic fox. Red fox generally don’t venture much above the tree line, but of course the Arctic fox does and actually reaches as far north as the high Arctic. All animal life has to start with vegetation somewhere. And of course, the Arctic fox can feed on lemmings., ptarmigan, voles, geese, and other migratory birds in the high arctic and even Arctic hares.

“It’s suspected that the warm estuarial waters also create a micro environment for the young whales who are born here.

With regards to the beluga whales, they actually will crossbreed with the narwhals. Researchers referred to them as narlugas. A hybrid between the two whales. With characteristics of both parents, but generally without a tusk. What I can tell you is the people who hunt them find it significantly harder to hunt the narwhals because they are considerably faster swimmers than the belugas.

The belugas have a migratory lifecycle migrating between areas known as Lancaster sound on the east side of Baffin Island and spend the winters in the high Arctic in areas where there is strong current and resulting open water. What brings them to this area is the brackish water environment, which is great for the fish that concentrate in the river mouths and provide for a quick layer of fat as the beluga’s will moult through the summer and require oily fish to build up the roughly 6 inches of fat layer around their bodies to help insulate them. It’s suspected that the warm estuarial waters also create a micro environment for the young whales who are born here.

PG: Many thanks for an excellent local flavour to this amazing and unique natural haven, Wally. May Churchill also transform intoan eco-tourism capital of the world.

In this interview, members of Teachers Against the Climate Crisis outline the Vision Statement for holistic, justice-focused, experiential, and nature-immersive climate education, calling for reforms in teacher training, curricula, and institutional structures.

Madhulika Banerjee (MB) teaches political science at the University of Delhi, India. Sonali Sathaye (SS) teaches Sociology and Theatre in schools and is a consultant on planetary health and sustainability at St John’s Research Institute in Bangalore, India. Vandana Singh (VS) teaches physics and environment at Framingham State University in the US.

PG: Could you please tell our readers about Teachers Against the Climate Crisis (TACC) and how the Vision Document on Climate Education came to be.

MB, SS, VS: TACC is a non-funded, non-party collective of over 120 teachers, scholars, academics and school teachers primarily based in India. We came together more than five years ago, out of our concern for the complex existential crises we face, and due to the paucity of discussion and action forums for climate education.

Very broadly, our aims are two-fold – among teachers, to deepen understanding of, and engagement with key aspects of the climate crisis: its science, impacts, systemic roots, state policy, political economy, and ways forward. Among students, we hope that such an improved understanding will catalyse more active engagement outside of the classroom and university, to demand the systemic changes needed at different levels to tackle the crisis. We have organized over 30 talks on various aspects of the subject. We also on occasion issue public statements on issues related to climate change and the environment.

Our Vision documentcame about through discussions within TACC starting more than two years ago. We three co-editors have collected thoughts and ideas from our membership, drafted multiple versions, obtained feedback from TACC members, and finalized the statement that we released in July 2025. The TACC Vision Statement on Climate Education is meant to be a living document, that is, we will continue to solicit feedback from the wider society and revisit the document at regular intervals. Our release event on July 19, 2025 sought feedback from five experts outside TACC and their comments will help inform the next version.

PG: What is your hope and motivation for the Vision Document?

MB, SS, VS: We hope this document will stimulate much needed conversations about what meaningful climate education is, why it is necessary, and what it entails. The unique aspect of the TACC vision statement is that instead of trying to fit climate education into existing frameworks, the frameworks that have failed us, we begin with the question: what does the climate crisis and related crises demand we do, as educators? And, as a group, we attempt to answer it. This entails examining the roots of the crisis and being able to distinguish lip service and greenwashing from genuine engagement with the polycrisis, which must be both just and efficacious.

It is our hope that those who engage with this document will use the material to find their own pathways to discussion/teaching…

Specifically, it is our hope that those who engage with this document will use the material to find their own pathways to discussion/teaching that work for their particular context, materially, socially and economically, and thereby enable them to connect with global processes. For example students could begin by examining the natural world (or lack thereof) in their own setting, or considering how waste is generated and disposed of. Students might visit a landfill or a trash pile and observe what kinds of waste are there, and what that can tell them about consumption/consumption patterns. This can be a jump-off point for exploring how this impacts the world beyond them.

Students could observe their local natural environments, the local species and the changes they are undergoing, and connect these observations with larger scale trends. Pathways to meaningful action could emerge from such local-to-regional-to-global interconnections. In fact, such pathways are already being worked out by groups of people in many different contexts – either community organisations working on specific issues like waste recycling or social movements demanding better interventions from the state. Our Vision Document recommends a deep study of such social-ecological movements so that educators and students can draw from them inspiration, hope, and ideas for their own pathways toward change.

PG: What does the document mean by ‘meaningful Climate Education’ and why is it necessary? What are the key aspects of the TACC Vision?

MB, SS, VS:Conventional education has failed us in the very important function of informing and preparing students for wicked problems like climate change. Much lip service is paid to environmental issues, climate action and climate justice, while the problem continues to get worse and worse every year. Here’s a quote from the document:

“Meaningful education should help create citizens who can think critically and ethically, question conventional ways of thinking, understand and contextualize current problems and issues, and collectively contribute their knowledge and creativity for the benefit of the world.” Our vision rests on four pillars that are essential to meaningful climate education:

1. It must be holistic and inter/transdisciplinary.

2. It must foreground justice and critique the current consumerist socio-economic system which is at the root of the climate crisis.

3. It must be experiential, action-based, service-based and connect the local to the regional and global.

4. It must be Nature-immersive.

The document elaborates on each of these, but briefly, what it entails is to recognize that the climate problem doesn’t exist in a vacuum, that it transcends disciplines, that it is related to other major social-environmental problems like species extinction, and that its root cause is inequitable, extractive and exploitative socio-economic system.

A “meaningful climate education” must demonstrate the intertwined nature of the current crisis.

Thus, a “meaningful climate education” must demonstrate the intertwined nature of the current crisis. This includes a solid understanding of the scientific processes that underlie the causes and implications of climate change – for instance, the nature of greenhouse gases, the links between various aspects of earth systems and the ways in which human activity has changed those systems. Students would learn how climate change is connected to other violations of planetary boundaries resulting in species extinction, chemical pollution, nitrogen cycle imbalance, etc., which constitutes a polycrisis rooted in our socioeconomic system.

This system entrenches systemic inequality in access to resources and opportunities, legitimized through long-entrenched patterns of custom and tradition (such as, for example, class, caste and patriarchy) along with increasing economic inequality and the legacies of colonialism (coloniality of power and knowledge). Students must therefore learn how issues of social justice and equity are inextricably intertwined with the crisis in the earth’s biogeophysical systems.

Educators have a responsibility not only to bring out these key aspects, but to re-imagine the classroom as a space where hierarchy and conventional wisdom are questioned, and where attention is paid to both the cognitive aspect of learning and the psychosocial aspects. This requires engendering collective agency among students through meaningful practical projects. All of this, of course, has major implications for teacher training. The document lays out seven recommended steps toward change in this regard.

PG: Despite well-established basic science and evidence – is it still business as usual (BAU) with regard to climate change?

MB, SS, VS: Given that the climate crisis and its attendant ills are not only getting worse every year but accelerating, it may be more accurate to state that we are beyond business as usual, at least looking at it in 2025. Despite some real (but inadequate) strides toward needed change, the problem is that global economies continue to operate on the basis of endless exponential growth that is completely at odds with Earth system boundaries. Although some systems have grown more efficient in terms of energy use (and with a burgeoning RE sector), the fundamental belief in greater consumption as a cornerstone of a richer life – and the inequalities that such an approach engenders – has not altered.

Global economies continue to operate on the basis of endless exponential growth that is completely at odds with Earth system boundaries.

Thus it is that climate emissions have gone up, not down over the years post-Covid, that the Earth has crossed the 1.5 degree C threshold set by the Paris Agreement in 2015 over many days of the last year – so that now scientists, politicians and businesses are talking of limiting warming to 2 degree C, which, even if we could reach it by 2100, would be likely to unleash a number of catastrophic feedbacks. The “circular economy” remains a distant dream. Our Vision Document needs to be read against such a backdrop.

PG: “These problems are particularly acute in the Indian context”. Could you please elaborate?

MB, SS, VS: In India, there are two broad dimensions of the acute nature that need to be a part of climate education. The first, is that the carbon-intensive nature of our industry and the chemical intensive nature of our agriculture have significant impact on those who do not have a say in making the decisions in deploying these processes, while there is a continuous powerful narrative of their value in national development. On the other hand, there are many, albeit scattered interventions of sustainable practices in all kinds of sectors, often by those that are neglected in the trajectory of development, and they remain without a voice.

PG: What in your view should students get from climate education?

MB, SS, VS: Students need to get the big picture of the interconnectedness of all problems across disciplines, as also the ability to understand the micro pictures at their local scale, and comprehend how the two are connected. At the same time, they need to recognise that there are multiple ways of knowing, and that certain local knowledge traditions can be both useful and inspiring. The real achievement of climate education lies in a belief in hope and action, rather than the cynicism and despair of the privileged – which is the case with a lot of the educated in general, the climate educated in particular.

PG: What are the recommendations in the document with regard to first steps toward change?

MB, SS, VS: Near the end of the Vision Statement we recommend seven ‘first steps’ toward change, which focus primarily on the teacher as changemaker. Because we have inherited from colonialism a siloed education system, it is necessary to train teachers in inter/transdisciplinary thinking and teaching, which, of course, requires high quality education research in this area. This also implies training in systems thinking, so that both the scientific understanding of climate change and the polycrisis and the sociopolitical implications can be elucidated. We call for training in Nature-immersive education at all scales so that students can have an experiential appreciation for the web of life to which we belong.

Because we have inherited from colonialism a siloed education system, it is necessary to train teachers in inter/transdisciplinary thinking and teaching…

None of these things is possible without addressing two major barriers, one of which is the hierarchical classroom structure, where the teacher is the ‘sage on a stage’ and where, in India in particular, societal inequities like caste, gender and religion can further exacerbate hierarchical divisions in the classroom. Beyond the classroom itself, especially for K-12 education there is a lot of pressure on teachers to conform, and the power differential at the larger scale cannot be ignored.

So, it is not just teacher training toward a radically different classroom dynamic that is necessary, but school administrators, principals, and university administration also need training in engendering and enabling flattened and shared-power structures. The second barrier is the lack of resources for teachers, especially in rural India, where poor compensation, lack of opportunities for training and motivation, and lack of materials are serious issues. So, we point out that these need to be addressed.

There are two other factors at the larger scale. One, we need radical curricular changes to accommodate transdisciplinary, nature-based education, so that anyone from any discipline can teach/ collaborate with a teacher from another discipline on climate change, and so that there is also room for overarching, cross-connecting courses that pull all the threads together. Two, we need to establish a tradition of high quality research on climate and environmental education in the Global South. Much of the work on climate education emerges from and is centred in the Global North, and the South needs our own experiments, conceptualizations and actions embedded in our own contexts.

But also, centuries of colonialism and the current crises are bringing into question dominant conceptualizations of climate change, and Global South perspectives on climate education can add fresh perspectives and ideas of benefit to the world.

PG: MB, SS, VS – Congratulations for an excellent articulation! This can be a playbook for what much of the world ought to do for addressing the biggest existential crisis we have brought upon ourselves.

Zaneta Sedilekova is Founding Director & CEO @ Planet Law Lab, London. She is a Biodiversity and Climate Risk Lawyer with a strong focus on risk and opportunities that climate and biodiversity crises present to the financial system as well as individual decision makers.

Zaneta helps clients understand and mitigate their exposure to biodiversity and climate liability risks, prepare for regulatory changes anticipated in the decarbonisation of worldwide economy. Most importantly, in her words, she helps clients turn these risks into opportunities.

Praveen Gupta: The ICJ verdict has either been received with lot of jubilation or dismissed as ‘non-binding’.

Zaneta Sedilekova: Both reactions are valid.

ICJ verdict is an advisory opinion, which means that it is only a non-binding guidance. In other words, no government or court is legally obliged to comply with it. Having said that, the opinion is a clear statement on how international law approaches the main questions related to climate change – it clarifies that under international law, all states have a legal obligation to mitigate their emissions, that a breach of such obligation especially by high-emitting states will entitle states who suffer from such breach to seek a legal remedy, such as compensation, and much more. Those are now principles of international law, and all states are part of international legal order. Ignoring these principles is not advisable.

“ICJ pronouncements will become legally binding as part of the domestic law.

This is where the jubilation comes in – this opinion is the clearest guidance we have on international law and climate change. While it does not bind any government or court, many governments use ICJ opinions as guidance when drafting policies and regulations. Courts are also often guided by ICJ’s opinions, not as binding law, but rather as an aid in interpretation and application of domestic law. And this is important – when domestic courts use this ICJ advisory opinion on climate change to clarify legal obligations of governments vis-à-vis climate change under domestic law, ICJ pronouncements will become legally binding as part of the domestic law. This is the true power of ICJ opinions on international law, and indeed, a reason for jubilation.

PG: Does it open floodgates? Young law students from a small Pacific sovereign state made it happen.

ZS: It definitely gives a boost to movement lawyering and climate litigation as many arguments made by ICJ can be used to build ambitious cases against governments. Policies and regulations, especially in relation to the fossil fuel sector, which do not outline transition away from production and consumption of fossil fuels, allow for continuous approval of new projects or indeed provide heavy subsidies to the industry, are all likely to face legal challenges from the civil society supported not only by science and, in some countries, national law, but also by clear statements of international law. That is significant. Impact of such cases against governments will cascade down the economy to corporate actors as well.

“Whether or not such measures are successful is not a question of the strength of law, but rather one of political attitudes and beliefs.

Whether or not we will also see more cases filed by states against states for climate reparations is a more open-ended question. International relations are a tricky area. As such international law, including binding ICJ judgments (rather than no-binding advisory opinions), is difficult to enforce given the absence of international police. States usually resort to self-help measures, such as sanctions and diplomatic pressure, or political dialogue, to enforce international legal obligations. Whether or not such measures are successful is not a question of the strength of law, but rather one of political attitudes and beliefs. Given the political volatility the world finds itself in right now, I do not believe that many positive results will be achieved in this way. At the same time, I hope I am wrong on this one.

PG: Are you enthused by the possibility of all the wavering and indecision getting a nudge (from this development) at the COPs on account of contentious adaptation and Loss & Damage issues?

ZS: I am not convinced that the ICJ opinion, however clear and unambiguous, is what is needed to nudge the COP negotiations forward. Ambitious law – in the form of the Paris Agreement – has been in place for a decade now. The progress has been made in that time but definitely not of the scale and ambition we need. The ICJ opinion clarifies that states’ obligations vis-à-vis climate change exist not only under the Paris Agreement, which is an international treaty, but also general international law, under what we call international custom. This binds all states, regardless of whether they have signed up to the Paris Agreement or not.

“Now we need international diplomats and politicians to get on that train too.

The ICJ also said that the breach of such obligations will lead to liability in the form of restitution, compensation and the like. With this all clear now, what is really needed is political will to move in the direction of enabling transition on state and international level, which includes the flow of adaptation finance, and in some cases damages, to states that are suffering the most. International law says this clearly, delineating, if you will, the direction of travel for the next few decades. Now we need international diplomats and politicians to get on that train too.

PG: Do you see this reinforcing a sense of hope amongst the upcoming generations?

ZS: Certainly. In the face of the political inertia that we have been witnessing for the past 10 years or so, having the top international court give clarity on important issues of climate change must be encouraging for young people. This is where the wider climate litigation movement really comes in – when people (of any age, I should add) feel that their elected political representatives are failing them, they turn to another branch of the power dynamics, the courts. The courts’ support of their arguments can only bring them hope.

“For the first time, having been ignored by their governments for years, the people feel heard and seen.

We have seen this in all high-profile climate cases in the past decade, not only the ICJ advisory opinion. It is almost as if, for the first time, having been ignored by their governments for years, the people feel heard and seen. Such is the power of public-led litigation. At the end of the day, the request for the advisory opinion was originally initiated by young students from the Pacific islands as a grassroot campaign asking for clarify in law and hope in life. They have now received both.

PG: Isn’t all this about integrating Nature into the ways of the state and business?

ZS: It is about finding a way to live in harmony with nature, be it as a state, business, or indeed the humanity at large. It would also help us all to see nature as an ally in this process – not as something we have to manage for our own needs, but as a greater wisdom, much older than our own, that shows us where we need to go. So, for example, the natural process of climate change points us in the direction of travel for our civilization – towards renewable decentralized and democratized energy system, small and mostly self-sufficient communities, more peer-to-peer trading and the list goes on and on. To answer your question then, I see it more as integrating states and businesses into nature rather than the other way round.

“If you accept that humanity is embedded in and dependent on nature, rather than the other way round…

PG: We are losing time and must act decisively. Will the verdict facilitate the much desired convergence between diverse societal aspirations and Planetary boundaries?

ZS: Acting decisively is important, I agree. The ICJ advisory opinion has put climate and environmental issues on par with social issues by framing climate change as a human rights matter. So indeed, it has brought forward what many of us knew for decades – that without a healthy planet, there is no humanity (healthy or otherwise). Convergence is likely to follow. I should also say though, that it is a matter of your worldview whether this is expansion and reduction of your thinking.

Climate change is a process that impacts everything on this planet – planetary processes and balances, entire species and ecosystems, and the whole of humanity. If you accept that humanity is embedded in and dependent on nature, rather than the other way round, the right question to ask is whether the ICJ opinion has contributed to reframing of the mainstream political and economic thinking, which sees our planet as a servant of humanity. I do believe it has and that we will see more development – academic as well as practical – on this question.

PG: Many thanks for these crystal clear insights and a strong sense of optimism, Zaneta!

Matthew Hill is the Chief Executive Officer of the Chartered Insurance Institute since April 2024. He comes with a rich and very diverse career path. Matthew studied Biochemistry at Lady Margaret Hall, Oxford.

Praveen Gupta: Increasingly, more and more European insurers and reinsurers are moving away from insuring and investing in fossil fuels. Would you expect this to be replicated globally?

Matthew Hill: The evolution of markets over the past few years has not been smooth, reflecting differences in political and public sentiment towards fossil fuel extraction around the world. For example, we saw a lot of firms in Europe withdraw from these markets between 2018 and 2023, but that wasn’t mirrored in North America, Latin America or Asia at the time.1 My reading of commentators’ views is that little has changed in the past couple of years that would suggest a further decline in participation in the short term, though there is also more talk about the adoption of novel solutions, such as self-insurance or expanding captive markets.

“I believe the sector is doing what it has always done well – reacting and evolving to the changing environment.

However, I think it’s equally important to look at the way in which our profession is supporting the development of new, greener technologies. We are seeing substantial growth in solar, wind and tidal energy along with storage capabilities. Insurance companies recognise that this is the long-term future of our energy needs and are facilitating investment in them around the world.

Novel technologies are not without risk themselves, but I believe the sector is doing what it has always done well – reacting and evolving to the changing environment. We’re proud to be playing our part in facilitating that change through educational initiatives, such as our Certificate in Climate Change, and by bringing experts together to discuss challenges and find potential solutions, as we did at the end of 2023 when we held a conference dedicated to sustainability.

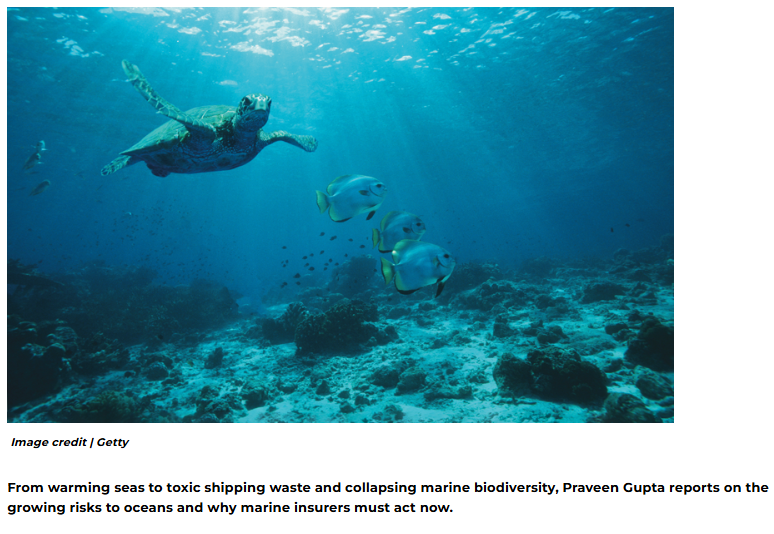

PG: Climate risk has a much broader scope entailing biodiversity loss and pollution. Are we ready to address the growing challenge with due urgency?

MH: The biggest challenge with climate change is uncertainty. Knowing the direct and indirect implications of individual actions for distinct environments can be hard. However, if any profession were well adapted to handling that challenge, it’s the insurance profession. Climate risk is necessitating the rethinking of traditional approaches to risk management, pricing and claims modeling, while the inevitable opening of some protection gaps is actually providing the incentive for existing firms and new entrants to develop novel solutions.

“The biggest challenge with climate change is uncertainty… However, if any profession were well adapted to handling that challenge, it’s the insurance profession.

We’ve seen some good examples of this in recent times, particularly with the development of parametric products that pay out automatically under certain circumstances. As such, I have no doubt that the insurance profession can find ways to support societies where it is desired. For me, the challenge is more around widening the conversation with policymakers and other stakeholders, so we all best understand the challenge we face and work together to find the right responses.

PG: Are we ready for yet another pandemic?

MH: I think the insurance profession proved during the COVID pandemic that it exists to serve society and is a critical enabler of resilience and recovery. It’s often said that the next crisis will be nothing like the previous one, so it’s hard to say whether anybody is truly ready, but it’s apparent that our profession has responded to the challenges encountered by individuals and firms at the start of this decade through the development of new forms of cover, such as the development, transit and storage of vaccines.

PG: With the arrival of #Polycrisis, don’t you think a new risk architecture is called for?

MH: I’m not sure the paradigm in which we now find ourselves has crept up on the insurance profession. We are a sector that is home to global firms, as well as niche specialists, who are all interconnected by brokers, underwriters and reinsurers that openly talk about the challenges and opportunities they face on a daily basis. Organisations like the CII help to further shine a light on the work of the sector by bringing participants together and distilling conversations and findings for other audiences, such as policymakers and the public. The openness with which we share information encourages debate and new participants to enter our market, who can bring fresh ideas, technology and ways of working. By implication, our risk architecture has been continuously evolving since insurance came into existence, and I think it will continue to do so in myriad different ways into the future, reflecting societal need.

“Organisations like the CII help to further shine a light on the work of the sector by bringing participants together and distilling conversations and findings for other audiences…

PG: Is Climate Change getting the due attention it deserves by insurance and risk management curriculum?

MH: There is no doubt in my mind that the insurance profession understands the severity of climate change. Annual natural catastrophe losses of at least $100 billion have become a fact of life, with no country seemingly immune to the impact of climate events. More than 40% of the world’s population now reside in climate-vulnerable locations and around 20% of global corporates are facing financial rating downgrades by 2035 due to climate vulnerabilities. The CII has held dedicated conferences on the subject, as well as developing new qualifications, CPD and practical guidance to help professionals understand and navigate the issues.

That’s not to say there is not more that can be done. The size of the challenge undoubtedly means that a societal response is needed, involving policy makers, regulators, technology developers and other stakeholders. For our part, in 2021 we introduced a dedicated Certificate in Climate Change. Since then we have had nearly 300 learners take the certificate, with broadly similar numbers (c70) in each of the past three years. The syllabus was reviewed and updated in 2023, and we will complete a further update in early 2026.

PG: Many thanks Matthew for these excellent insights. My best wishes for your leadership in these challenging times.

FUTURE SHOCK byAlvin Toffler& his wife Adelaide Farrell has stayed as a playbook for me in terms of insurance industry’s tech trajectory. While the authors did not call it AI, they envisioned how far tech would aid human advancement. Needless to mention all the cautionary advice packaged in – to ensure we do not abdicate to it. “Our choice of technologies, in short, will decisively shape the cultural styles of the future,” Toffler once cautioned.

The industry audience I had the pleasure of interacting with recently – courtesy CII HK – gave me the confidence that they know when to say STOP!

And how can I not acknowledge the power of a gift. This book came to me from a dear friend just as I started my hesitant career in insurance. It has disappeared and reappeared as I have moved homes and locations. Its pages yellower each time I look it up. However, the intensity of how it continues to fuel my imagination is a constant.

Blair Palese is Director of Philanthropy at Ethinvest and founder of the Climate Capital Forum, a network of investors, decarbonising businesses, climate finance experts and philanthropists advocating for Australia to lead in the global net zero economy. She is also co-founder/contributor at Climate & Capital Media, a global online outlet covering emerging climate opportunities.

Blair founded and was CEO of 350.org Australia for ten years from 2009 and has worked for companies, government programs and not-for profits in the climate and environment space, including the Google X Moonshot team, C40 cities for climate action, The Body Shop with founder Anita Roddick and as communication director for Greenpeace International and Greenpeace USA.

Praveen Gupta: Australia is one of the world’s most vulnerable countries to climate change impacts, facing ever-worsening droughts, bushfires, flooding, and rising sea levels.

Blair Palese: More than most nations in the world, experts say Australia is highly vulnerable to climate change impacts – drought, flooding, extreme weather and fire. This means we need to reduce our emissions and move rapidly away from polluting fossil fuels to clean alternatives not only for our climate, economy and energy security but to try to mitigate the incredible costs of these growing impacts. The insurance costs from the Black Summer bushfires in 2019-20 for instance affected 80% of Australia’s population and caused A$2.4 billion (US$1.5 billion) of insured loss according to Moody’s. The Insurance Council of Australia says the insured losses from two extreme weather events, including deadly flooding in the New South Wales mid-coast, have already reached A$1.5 billion this year. Addressing climate change makes sense not only for a liveable planet in the future but for a vulnerable Australia.

PG: Congratulations for rejecting climate denial! How do you believe will the current government utilize its mandate to intensify the climate action it has initiated?

BP: It certainly was a win – especially when polls just weeks before the election suggested a very close race. We are fortunate that, despite the incredible power of the fossil fuel sector in Australia, the re-elected Labor government “gets” the opportunities of becoming what it likes to call “A Renewable Energy Superpower.” That means not only continuing to move to renewable energy within Australia – we are averaging an impressive 46% in our grid and occasionally reaching up to 75% renewables according to our energy regulator. It also means ramping up the development of net zero products such as green iron ore and steel, to countries that need to buy net zero in to meet their targets — China, Korea and Japan.

Albanese’s Labor government committed A$22.7 billion to a range of Future Made in Australia initiatives and incentives in 2024 – something my Climate Capital Forum advocated strongly for over three years. This included incentives for everything from Production Tax Credits and renewable energy hubs to support for green hydrogen and critical mineral mining development (full list below*). One of his party’s most important steps was announcing a home battery incentive scheme of A$2.3 billion for Australian homeowners, particularly the one-in-three that already have solar power and want to back that up with batteries. Voters sent a strong message that they back this and want more.

Our country’s real challenge, and where Labor leadership is sorely lacking, is developing a strategy to wean our export market away from coal and gas and toward the net zero products…

It’s a vast improvement on the previous Coalition (Liberals and Nations, both conservative) government, that proved itself to be irrelevant in the last election by promoting highly expensive and hugely unlikely nuclear power from a cold start — largely seen as a ruse for extending gas and coal use. It was a key reason the Coalition suffered one of its biggest election setbacks in Australian history.

Our country’s real challenge, and where Labor leadership is sorely lacking, is developing a strategy to wean our export market away from coal and gas and toward the net zero products above. Labor is still approving new gas and coal projects such as its recent approval of Woodside’s North West Shelf gas project to 2070. This and the 30 odd fossil fuel approvals Labor’s made since its 2022 election win contradict the IEA’s no new fossil fuel projects if we are to meet our global 1.5C emissions targets mandate. There is much more work to do here and we are up against all too powerful fossil fuel and mining political power keen to prevent that from happening.

The economic stakes are high. It’s time for the Labor government, with a mandate that might possibly give them six or more years in power, to pick a side and that side is net zero, not fossil fuels. Investors, businesses, importers and innovators need certainty and the government needs to provide it.

PG: Do you believe Australia is on track to become the world’s first climate superpower? Do you see efforts in place to increase renewable energy supply to 82% by 2030 and 95% by 2035; net-zero steel and iron ore; emergence as the global champion of exporting net zero?

BP: It’s a real possibility BUT that export transition challenge is a big challenge along with our lacking a startup, innovation culture that would allow us to move fast enough to take a seat in the growing net zero global market. My network, the Climate Capital Forum, and associations like the Investors Group on Climate Change are working to encourage the Australian government to learn from initiatives like those in California, the US’s IRA, Europe’s carbon price and renewable energy incentives and other successful climate financing approaches to put them in place fast and get moving. With Trump’s America leaving the field, there’s a huge gap Australia could fill if we are able to kick-start the innovation and use the incredible renewable energy and critical mineral resources we have – many would say, the envy of the world.

PG: How inclined are the money pipelines (banks, insurers, fund managers) to fine-tune with your climate aspirations?

BP: We really need the federal government to continue upping its financial and policy support to send a clear message to private investors here and overseas that this is where Australia is going. With the outcome of the election, we have three and a half years – maybe more – to lock in our efforts to become that Renewable Energy Superpower the government likes to talk about. Our investors, banks, funds managers and insurers are conservative by nature. They will need policy certainty and funding from the government and its programs like the Clean Energy Finance Corporation (CEFC) and Australian Renewable Energy Agency (ARENA) to help investors to see the opportunity and crowd in private funding to make this work.

PG: Given your climate vulnerabilities, how receptive are you to the Indigenous intelligence and practices?

BP: Sadly our First Nations communities have often been left behind in the effort to move to clean renewables but organisations like Original Power and its First Nations Clean Energy Network are changing that for the better. The First Nations Clean Energy Network is supporting more than 20 Aboriginal communities around the country to fund, install, own and run their own solar power systems and get off of polluting and expensive diesel. Their work really shows how it can be done well to ensure everyone benefits from the transition.

PG: How was your recent trip to Tiwi Islands and the interaction with the elders?

BP: It was such a privilege to be invited by the Elders of the Tiwi Island community of Pirlangimpi who have been trying to stop Santos’ Barossa offshore gas development just off their coastline. Sadly and unbelievably, they only found out about the development plans long after they were underway. There was no consultation. In 2022 Tiwi Elders took the offshore gas regulator to court, on the basis they had not been properly consulted and won in a landmark ruling that has had broader implications across environmental rights advocacy. In 2023, they lodged human rights grievances against Australia’s banks for their continued financing of fossil fuel extractors, and a delegation of elders recently travelled to Japan and South Korea to meet with key financial backers to argue that the community opposes the project on cultural and environmental grounds.

It’s a David and Goliath battle and an example of the centuries-old tactic of cashed-up corporates going into first nations communities, driving a wedge …

Sadly, they lost a key court case in 2024 against Santos on cultural heritage grounds. The company plans up to seven gas projects, one as close to 50 kms from the Tiwi coast, for export to Asia, and the community getting zero benefit and all of the impact. Santos exports 80% of its Australian-generated gas for profit offshore, pays extremely low income and resource taxes and can afford multi-billion-dollar US law firm, formerly a Trump firm, Quinn Emanuel. It’s a David and Goliath battle and an example of the centuries-old tactic of cashed-up corporates going into first nations communities, driving a wedge – usually by offering cash to those least impacted to support the project to get what they want. It not destroys the environment but often the first nations communities as well. Additional legal action is likely and the battle isn’t over yet. Labor’s leadership will be called into question here. For more information, see Jubilee Australia, who are working with the Tiwis to support their effort to stop Santos.